.png)

"When it's your time, it is your time." — Bruno Mars.

Mar 31, 2026

(Return figures come from the March 31, 2026, edition of the Wall St. Journal. Y H & C Investments may have positions in companies mentioned in this newsletter. Nothing in the newsletter should be taken as an offer to buy or sell individual securities. It is the responsibility of each investor to research the investments mentioned so they can decide on the appropriateness and suitability of the investments consistent with their risk tolerance, risk constraints, and return objectives.)

Indiana University officially hired Curt Cignetti as its new head football coach on November 30, 2023. In the prior 18 years, Indiana had winning records in just two of those eighteen seasons. As most observant college football fans will tell you, Mr. Cignetti’s transformation of one of the perennial losing programs is considered at the very least a legendary accomplishment. Some rank it as the greatest coaching accomplishment ever. The brief clip below at his initial press conference sums it up nicely:

“It’s pretty simple. I win. Google me.” How can you not love that description? More importantly, he went out and proved it, and last year won the national championship with an undefeated season. Legendary stuff. So, why does this matter for investors?

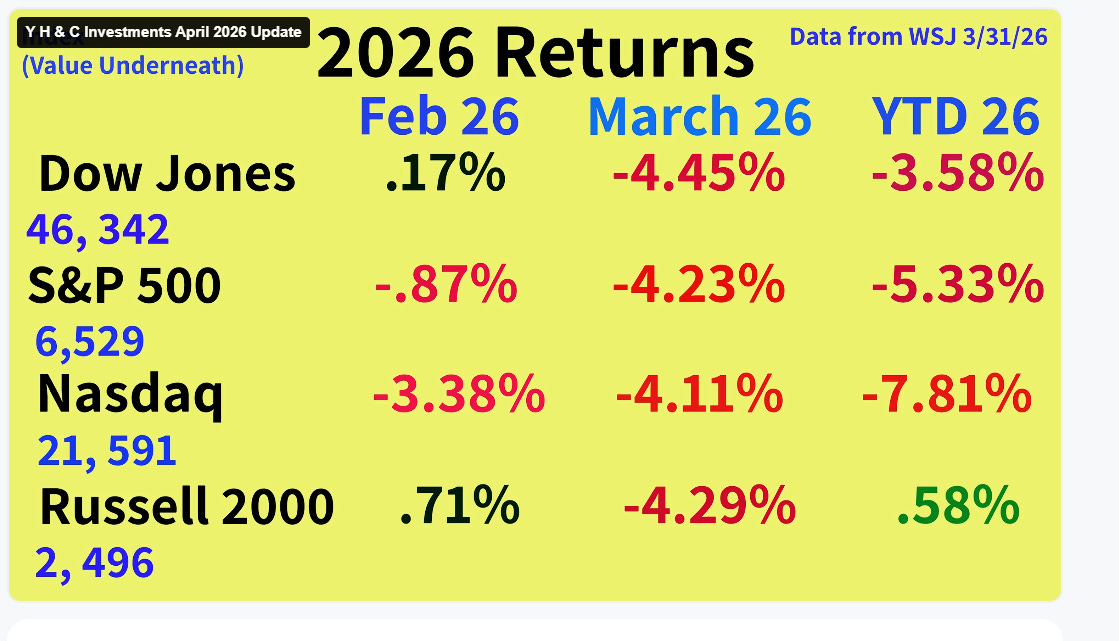

With the equity markets in a five-week losing trend, the selloff has been quite difficult for many companies. If you are a long-term investor, the recent environment is nothing out of the ordinary. Most U.S.-listed stocks have suffered from a dearth of interest over the last fifteen years. The small and microcap area continues to face the problem of a lack of buyers because of that issue. The most successful equities over the last decade were found in software entities with superb growth records compiled over many years. They, too, fell prey to the flightiness of institutional capital and have sold off quite hard over the last three months. During the outset of the year, gold and silver companies had tremendous runs, but, alas, have taken it on the chin and sold off in the last thirty days. The recent difficulty in equity markets highlights the potentially treacherous terrain that sometimes engulfs capital markets. One could easily point to the cause of the travails, which is the war in Iran. The change in oil prices and the related thought that maybe interest rate cuts are now off the table, and potentially rate hikes are now possible as the prime reason for the recent heavy selling. Is there anything we can look at and say, yes, this has worked? For sure.

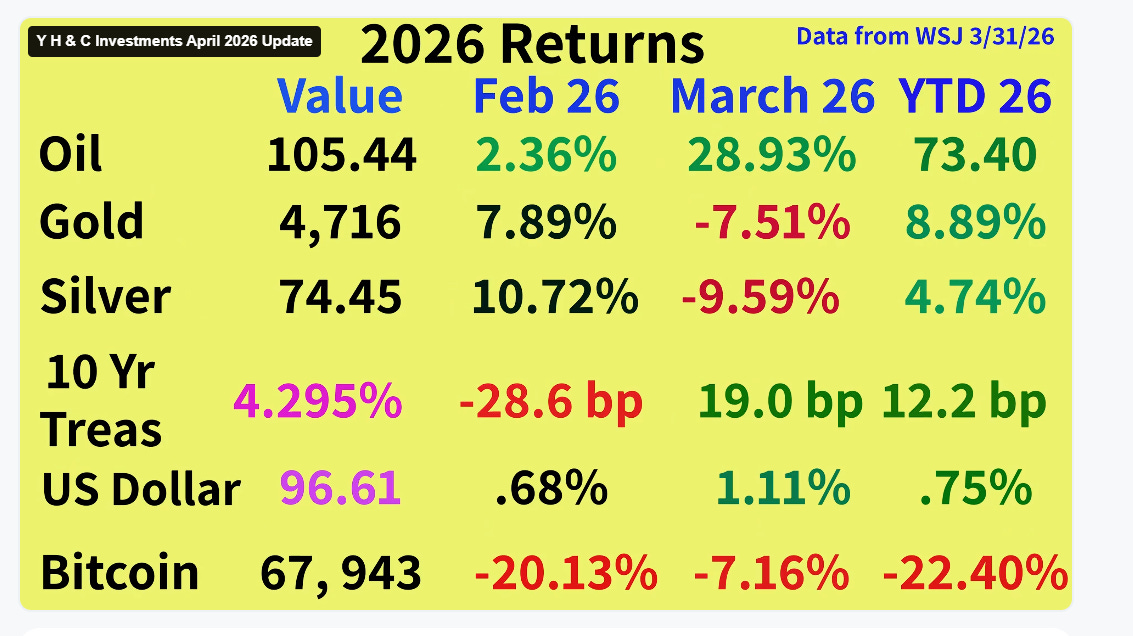

Without question, the prime beneficiary of the current situation is the energy sector. For those not paying attention, black gold has rocketed higher from $60 per barrel of Brent to somewhere north of $110 as I write this. The term energy is a vague term as there are many different energy forms- oil, gas, liquified gas, coal, solar, wind, nuclear, geothermal, and biofuels. What is most misunderstood about the energy area is that there are several aspects of energy you can own. For our purposes, let’s narrow things down to any type related to oil and gas. For those unfamiliar with the industry, the effort to extract and then generate is exploration and production. Changing the form of the underlying material and then moving it and selling it is refining, storage, pipelines, shipping, and marketing. Each has its own unique characteristics, but many investors find the industry too capital-intensive or complex to invest in. I would argue this is true in some pieces of the complex, but not so much with others. The one difficulty with it is that it is viewed as being dependent on the price of the underlying commodity. With a little over one hundred million barrels of oil per day consumed across the globe, the last decade has seen many producers spend less money on replacing and adding to their existing reserves. Typically, in any year, about 5% of the existing resource base needs to be replaced. If you curtail spending on extraction and have natural depletion, what you own is going to slowly trend lower.

The conflict in Iran brings the matter of logistics into the equation. Iran has long controlled the critical shipping area known as the Strait of Hormuz. It is a narrow chokepoint that connects the Gulf of Oman and the Arabian Sea. It serves as the sole sea passage for over twenty percent of global seaborne oil. With Iran taking the posture that no oil will pass through this area without it being the traffic light on what passes and what does not, the world’s countries are essentially having to answer to a regime that has historically been hostile towards not only America and Israel, but many other countries across the globe as well. Not a sustainable situation in any way.

From an investor standpoint, this kind of situation is why energy needs to be a part of a portfolio. Nobody has any idea how this will play out, though my feeling is that it will eventually be resolved. It might be in terms the world can accept, maybe a little tougher, maybe a whole lot better. Regardless, energy is something people must have, like healthcare, utilities, shelter, food and beverages, and transportation, among others. You don’t know when you get a great return, maybe never in all likelihood, and what causes it. You only know it is worth owning and continuing to own. Energy investors have waited a long time for their moment, so there is merit in what Bruno Mars said.

Share Y H & C Investments Weekly Blog & Monthly Newsletter

Spanning the Globe: The Implications of the Conflict in Iran

The world is focused on the conflict between Iran and the United States. What the outcome looks like is the crucial question for the entire world. It seems clear that Iran’s military capabilities are in the process of being severely degraded for a long time. The prime reason for the attack was the nuclear ambition of Iran. The issue of Iran’s existing uranium and whether it is still available for enrichment in the future remains a high priority for the United States and Israel. If Iran is still in control of this energy source and the existing leadership remains in power, they will continue to pursue their nuclear ambitions.

The second key issue is how much of Iran’s military capabilities remain intact, specifically their ballistic missile arsenal. With daily launches toward Gulf countries and Israel, the idea that any population has to spend every day running in and out of bomb shelters is not going to work. In combination with nuclear ambition and ability to deliver it, Iran could potentially rebuild and strike, unless this aspect of its military operations is eliminated.

The third major item is the question of access through the Strait of Hormuz for global shipping. With so much oil and gas around the region affected by this critical area, who is in control, what the security situation is, and what the terms for access are are all questions that remain unsettled. The major countries of Asia, (China, India, and Japan), as well as the mature ones in Europe, especially the UK, Germany, France, Italy, and Spain, are all vulnerable to any disruption of oil and gas supplied from the Gulf. Interestingly, when the US asked for financial or military help in managing the Strait of Hormuz bottleneck, these countries were reluctant, if not dismissive, to participate. In the event the US attempts to take over or disrupt fuel from Kharg Island (home to 90% of all Iranian oil and gas exports), or the other small islands in the Strait, which serve as the toll bridges for transport, these countries will certainly need to reconsider this posture. How will this be resolved? It is the multi-trillion-dollar question.

All these critical questions are dependent on who the leadership of Iran is. As of right now, it is anybody’s guess as to who is running the country. The existing leadership appears to be the IRGC, as most of the prior leaders have been killed. This is still an extremely authoritative group that recently not only killed over thirty thousand of its own citizens merely for protesting existing country conditions, but proceeded to charge family members thousands of dollars for the right to look for their bodies. In the event of a leadership change, it could bring drastic changes across the region and globe. Time will tell how this plays out.

Y H & C Investments Firm Update- Energy Wins, Reinvesting REIT Proceeds, Microcap Results, and the AGM Trip.

March has been a challenging month for most investors, as not much has worked other than energy. On that point, our portfolios have long maintained exposure to integrated energy companies and refining and marketing entities with logistical advantages. These holdings have worked extremely well over the last few months. Across our other positions, especially larger entities, the negative trend in the market for anything other than energy makes for a very stiff headwind. Still, much has held up well, especially in the real estate area. The buyout of our Hawaii-related REIT closed, and I took the proceeds and reinvested in another REIT. REIT’s come in a wide variety of specialties, sizes, and management structures, and there is plenty to look at. The attractive characteristic of many REIT’s is the income they generate and pass on to holders. Conversely, the weakness of the structure is that the IRS mandates that 90% of the net income proceeds are distributed to shareholders. It makes reinvesting in the business quite challenging when looking to grow the value of the enterprise.

A few of our larger microcap holdings reported fourth-quarter earnings in March, and the results were as expected. My observation with many microcap positions is that aside from management and the competitive dynamics and of the business, the most important piece of information for investors is what is called the cap table. It tells you which entities are the largest holders of the stock. The largest problem with this part of the market is that there is a dearth of capital invested. It is dominated by retail investors, with some hedge funds, and a few small, adventurous family offices and institutions. You must expect massive volatility with these names, and 30-50% swings can happen in a day or two. It certainly is not for those with weak stomachs. If the cap table consists of entities that aren’t constantly trading in and out, it certainly can provide stability. The same holds for the executives. In many cases, long-tenured executives take every opportunity to ring the cash register when the stock just starts to perform. When the management team is consistently putting their money where their mouth is and buying stock in the open market, it lends credibility to the case that they are long-term owners. Over the last week, I traveled to Florida for an Annual General Meeting of a large holding. It was well worth the time spent, and every time I go to an AGM, I learn more about a company than those who don’t attend.

Interactive Advisors GARP Models-

In March, the Concentrated GARP model was down slightly, which is not a great result but not bad. As mentioned previously, the REIT deal closed, and I reinvested in another REIT, which is run by someone whom I consider the best real estate investor in the world. Our energy holdings bolstered the portfolio. The rest of the holdings faced the headwinds of a market only interested in black gold.

In Long Term GARP, the portfolio increased nicely as energy bolstered our value, as did a continuing rebound of our large tax and financial services holding. The rest of the portfolio faced headwinds, especially in anything consumer-related. Still, any time your portfolio is up when the market is down by nearly 8% for the month, you must feel ok about how it performed.

For more information on the models-

Y H & C Investments: Concentrated GARP Investment Portfolio - Interactive Advisors

Y H & C Investments: Long Term GARP Investment Portfolio - Interactive Advisors

Share Y H & C Investments Weekly Blog & Monthly Newsletter

Thank you for reading the April update. I really appreciate it. if you have any investment questions, please reach out to me at information@y-hc.com.

.png)