.png)

Something out of nothing-

Jul 31, 2025

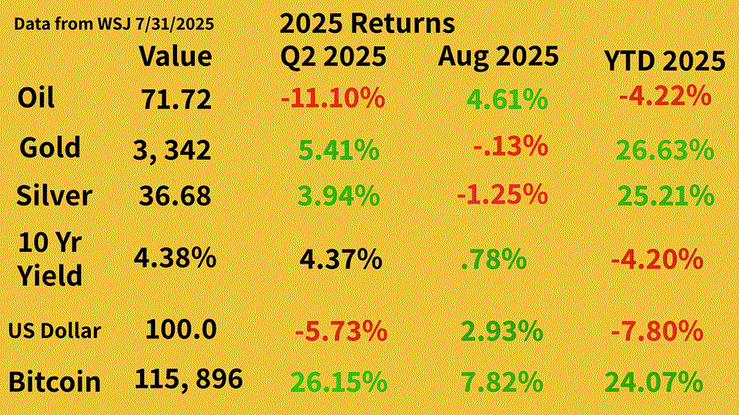

(Return figures come from the July 31, 2025, edition of the Wall St. Journal. Y H & C Investments may have positions in companies mentioned in this newsletter. Nothing in the newsletter should be taken as an offer to buy or sell individual securities. It is the responsibility of each investor to research the investments mentioned so they can decide on the appropriateness and suitability of the investments consistent with their risk tolerance, risk constraints, and return objectives)

The famous saying,” It is not over till it is over,” is typically applied to sports. Many fans have experienced a situation where the game is at the very end and one team is leading and all they have to do is finish the game with a final play to close the contest. Yet, the decisive moment often brings unpredictable endings that reverse which team ends up victorious. In many of these situations, one team appears dead. Done. Cooked. Forget about it. The video above is from the 1977 National League Championship between the Los Angeles Dodgers and the Philadelphia Phillies. Both were legendary teams with well-known players. Each ultimately wound up winning a world championship in a later year. The Dodgers were my favorite team, and I was only ten years old, but I remember this game vividly. Nothing was happening. The Dodgers were dead, and the Philadelphia fans smelled victory. They were down to their last out and were trailing by two runs. They bring up a pinch hitter named Vic Davalillo, who I am pretty sure nobody has ever heard of. He gets on base with a drag bunt, and the Dodgers proceed to score three runs, take the lead, and win the game. So why do I bring this up?

In the business world, quality management teams have the ability to find ways to create value in unforeseen ways. It is often the case a company is viewed by the investment world as having limited growth prospects. Meanwhile, management is in the process of working on ways to completely change the business. One prominent example is when Apple had just been taken over by Tim Cook and was seen as a one product company with the iPhone. It was thought its best days were behind it because the growth of phone and tablet units was slowing. Over the next decade, products like a watch, air pods, subscriptions for music and video content, and payments from the Apple Wallet have added many billions of dollars of revenue for the company. Add-ons like insurance and warranties bring in more revenue. Investors who bought the stock when the sentiment was terrible were rewarded.

Another prominent example was Microsoft after it changed leadership and brought in Satya Nadella. He changed the focus of the company in a number of ways, including a heightened priority towards the cloud and enterprise segment and a more aggressive posture regarding capital allocation. Microsoft acquired LinkedIn and Activision and now appears well positioned because of its ownership and relationship with OpenAI (owner of ChatGPT). In the quick service restaurant area, both McDonald’s and Chipotle were in situations where the business was thought to have minimal growth prospects or trouble. New leadership was brought in and, over time, the businesses rebounded and flourished. Personally, the example which impacted me the most is what Liberty Media has done with its equity pieces of various assets over a lengthy period of time. They had minority but prominent ownership in a wide variety of businesses. Liberty focused on a few areas where they had experience and could influence operations. In the cable business it is with Charter. In the satellite business, it was with DirectTv and SiriusXM. Looking at related areas, their holdings belong in the sports and media segment and include Formula One, Live Nation, and the Atlanta Braves. Finally, Liberty still owns the worst performer, which is the retail business of QVC. In terms of turning nothing into something, the Braves were a throw in as part of a deal with Rupert Murdoch. The Formula One stake was the byproduct of a lawsuit settlement with Vivendi. Liberty took those assets and made them into much stronger businesses with operational excellence.

My point for investors is management quality is always mentioned as a critical aspect for buying into a company. The description management quality, or high-quality management, is very vague, so let’s be more specific. High quality management is able to assess the resources of the company and find a way to work with those assets to unlock and build value. It usually does not happen in a week or two, or a month. Often it takes three to five years or more. Maybe assets are sold, and the cash is used to reposition into a different business. Let’s take the case of Berkshire Hathaway, which was a cash and receivables rich textile company when Buffett bought it. In what was probably their most important move, they used the assets at Berkshire to enter into insurance, buying National Indemnity in 1967. Buffett and Munger then changed their ownership within Berkshire to get out of textiles and move towards branded consumer products like See’s Candy and then a billion-dollar investment in Coca-Cola in 1988. After the National Indemnity and See’s purchases, Buffett owned profitable businesses that provided him with consistent cash he could then deploy into stocks or buy more profitable businesses. In the case of Liberty, deals to swap minority positions into controllable assets in a tax efficient way are the standard method. The ability to make something out of what appears to be nothing is not just important in sports. In the business world and investing, it probably is even more critical. It is never over till it is over.

Spanning the Globe: Trade Deals, Deals, and the Genius Act

Over the last month, the most noteworthy business news centers around the ongoing negotiations between the United States and global countries regarding tariffs. It appears the United States is on the path to completing trade deals with the largest countries and regions in the world which will change the terms of trade between the respective areas. The most prominent announced deals are now with the UK, Japan, and the European Union. The European Union agreement sets import tariffs into the United States at 15%, higher than the UK tariff of 10%, but lower than the threatened rate of 25%. Clearly, each situation is different, but the Trump Administration has a priority to create more opportunity with foreign countries by equalizing trade terms on exports from the United States and imports from other countries. August first has been the drop-dead date for deal finalization, but with negotiations anything can be moved back or changed. I suspect the world and investors will have this behind us at year end.

In the United States, the Trump administration has been extremely aggressive in announcing investments into specific companies to help the country compete. Specifically, rare earths is an area where national defense, car manufacturing, electric vehicles, robotics, and electronics are all dependent on those critical elements. One could imagine more of these direct investments by the Trump Administration into strategic areas. The largest target of these expenditures is probably in the energy area, most heavily related to oil and gas. The nuclear industry qualifies, and plutonium may be on the radar. There is probably a good possibility it could also take place in the digital domain as well. On that front, the Genius Act was signed by President Trump. It centers on stablecoins and payments. There are a few key takeaways from the bill, but the big one is the tremendous latitude and discretion given to the Treasury Secretary. It empowers him to help create the structures and legal protocols for banks and other financial entities to integrate stablecoins into the banking system. Here is an article from the Financial Times which brings up staking, or lending in the crypto and stablecoin space, and how it is starting to proliferate- Crypto lenders dial up risk with ‘microfinance on steroids’

Y H & C Investments Firm Update-

A standard method of real estate and financial services investing is comparing your borrowing costs to the returns from what you are buying. As an example, try to borrow low, let’s use 5% as an example, and earn more than 5%, hopefully much more, like 8-10% or better. It is called spread, and the larger the better. Where there is trouble is when you borrow at 8% or more, and your return is 5% or less, well, that math isn’t going to work. It is why there is always opportunity because what is projected doesn’t always turn out. A big part of investing is understanding what you get versus what you pay.

Related to the theme of turning nothing into something, there is the situation where one starts with something and uses the something to create more value. Across our holdings, real estate is an area where some of our companies are applying this tactic. The largest case is where a holding recently bought a portfolio of net lease properties for $2.2 billion. The assets comprise 467 units spanning 12 million square feet and are 100 percent leased. The lease terms are for nearly 20 years and have 2.2% annual rent gains (offsetting potential increases of inflation). For the purchase, if one assumes a 5% yield, the cash flow yield from the assets should incrementally increase earnings by at least $100 million. The sprawling REIT has a large lending business, so this changes and diversifies the earnings stream. It was funded in part by issuing a little over 500 million of stock, which amounts to dilution of about 7%. Another holding took its biggest industrial asset and is redeveloping it into a larger project where three quarters of the new space is pre-leased. In combination with another 75-year ground lease announcement, this company is clearly working on using their existing assets more productively. Finally, another holding earlier in the year sold a retail mall and took the proceeds to buy multifamily housing in an area which is logistically more attractive.

Over the next few weeks, many of our larger holdings will be reporting their quarterly results. The largest bank and tech companies have posted strong numbers and quite a few of the strongest global financial companies have dramatically increased their dividends after passing the government stress tests. Interestingly, the tech companies are famous for the quality of their business models, but now circumstances are changing. For many of them, massive capital expenditures have dominated their conference calls with the spending in the tens of billions of dollars. Those companies have plenty of cash, but ultimately the question becomes the return on the capital expenditures. Investors will be focused on that issue for a long time.

If ever there was a leader who turned nothing into something, it is Jamie Dimon. After helping Sandy Weil build Household Finance from the dirt into Citibank, he was then fired by his mentor. After a year of sitting out and evaluating opportunities, he took the helm at Bank One, a third-tier bank and credit card entity based in Chicago. Not for long. Dimon cleaned up the mess at Bank One, merged it with JP Morgan, at the time also a second-tier financial entity, and then proceeded to conquer Wall Street by a factor of ten. For those of you so interested, here is an excellent interview with Jamie Dimon, who is really the king of the financial community.

In the smaller company area, one of our holdings related to the electric grid area announced several nice wins with existing customers. In our little neck of the woods, a small legal tech firm just announced an investment of $450 million to refocus on crypto and stablecoin lending and recovery. One other point is that last month in the update I noted that returns for stocks typically come in bunches. Relatedly, the cover story of Barron’s mentions one of the largest media companies and how the stock has gone nowhere for ten years. On an excellent podcast- The Real Eisman by Steve Eisman (of The Big Short fame), he brings up the two largest telecom companies who have the same situation.

Finally, in the shameless promotion category, I am including a few videos for the models I run at Interactive Advisors. Once in a while it is good to remind people of what you are doing. Here is a link to the Interactive Advisors site.

For those of you interested, both models’ minimum investment is $100, so it enables a very low threshold to invest in what I believe are excellent companies and do so on a continual basis. Here are the videos for the models-

Let us not forget- links to the model pages-

Y H & C Investments Long Term GARP Model

Y H & C Investments Concentrated Long Term GARP Model

Thank you for reading the August update, I really appreciate it. If you have any investment questions, please reach out to me at information@y-hc.com.

(Y H & C Investments may have positions in companies mentioned in this newsletter. Nothing in the newsletter should be taken as an offer to buy or sell individual securities. It is the responsibility of each investor to research the investments mentioned so they can decide on the appropriateness and suitability of the investments consistent with their risk tolerance, risk constraints, and return objectives)

.png)