.png)

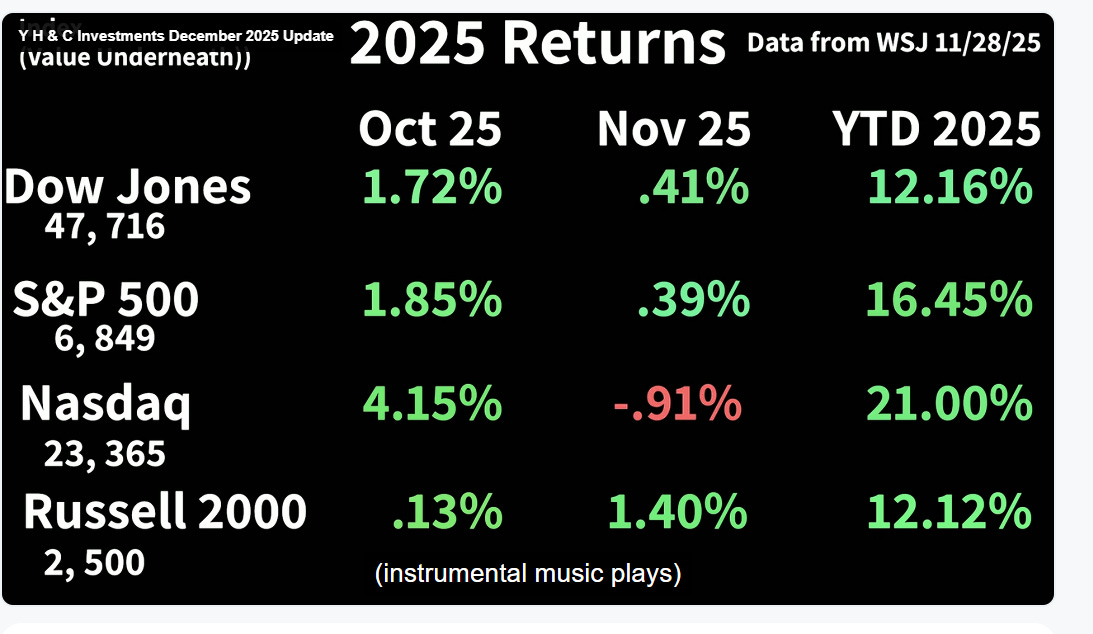

(Return figures come from the November 28, 2025, edition of the Wall St. Journal. Y H & C Investments may have positions in companies mentioned in this newsletter. Nothing in the newsletter should be taken as an offer to buy or sell individual securities. It is the responsibility of each investor to research the investments mentioned so they can decide on the appropriateness and suitability of the investments consistent with their risk tolerance, risk constraints, and return objectives.)

“All men can see these tactics whereby I conquer, but what none can see is the strategy out of which victory evolved.” ~ Sun Tzu

Coaching and investing are similar because both have specific results an organization is trying to achieve. I coached basketball in junior high school, high school, junior college, and aided a major college program. With coaching, you are trying to have a positive life experience for student athletes and win games. If you are paid to coach professionally, it is simply to win games.

The approach is your strategy for victory. Many coaches view this as playing better than the other team. Others set about by making fewer mistakes than their opponent. The specific tactics a team uses apply to the kind of offense and defense that are employed. On offense, the goal is to play together in a way that allows for high-quality shots without giving the ball to the other team. There are many forms of offense one can use, but everything leads to playing together and not turning the ball over. On defense, the objective is to make it as difficult as possible for the other team to score. On defense, there are two formats: man-to-man defense and zone. Theoretically, by employing man-to-man, if each player does an excellent job, the opposing team will have no weakness to attack. In a zone, there is always a shortcoming. In practice, both have vulnerabilities, but I believe the best chance of success is playing man-to-man. Regardless of the tactic, fundamentals like moving your feet, cutting off certain areas like the baseline, being physical and aggressive without fouling, and helping other teammates should all result in the opponent taking off-balance and contested shots. Your fundamentals on offense and defense are worked on every day, and when the team understands and improves at these basic concepts, it gives the organization the best chance to win games. Ok, great, so how is this like investing?

Investing is the process of allocating capital today to achieve more capital in the future. There are different ways this can happen. One is with some form of income that you receive by owning an asset. A second is having an underlying asset go up in value. A third approach is to sell an asset today to buy it back at a lower price. This is called ‘going short.’ Some combination of the three is employed by investors in nearly all instruments. These are the desired outcomes. The tactics for investing are infinite because investing is a subjective activity. Each entity views it in its own way and has its own background, knowledge, and skill set. My goal is to own high-quality businesses for the entities I manage money. A high-quality business will grow its revenues and profits over an extended period of time from x to two x to three times x and beyond. These entities have unit economics where the business will earn a return on capital higher than its cost of money. As an example, if capital costs the business 6%, the returns are going to be much higher than this, let’s say 12-20% or more. As the business makes profits, it deploys them so the enterprise will generate greater revenue and earnings in the future. The entire process can take place in any industry anywhere in the world. Investing is like coaching because in both, you are using an approach to achieve specific results that are definitive. Let’s turn our attention to what is currently taking place in the capital markets today.

With 40% of the S&P 500 value attributed to seven companies, the index is heavily dependent on these entities. Quite a few of these enterprises are the largest participants in the artificial intelligence industry. Investors own these massive companies, which have experienced tremendous growth over the last few decades. Their values are in the trillions, reflecting the excellence of the businesses, and potentially much more. As such, investors have a simple choice to make. Do you want to own these businesses, either individually or through an instrument like the S&P 500 index? As an alternative, would you choose to own other enterprises that are not these dominant businesses and are not the largest players in artificial intelligence? You could own the other 490 or so companies in the S&P 500, or any one or more of the thousands of other publicly traded companies across the globe. They could be of any size or in any industry. This is the key question for investors in deploying capital for both the short and long term.

The goal of investing is either generating income, having assets increase in value, or some combination of the two. Like a coach who trains the team each day to play the game their way, an investor allocates capital using their preferred strategies. One can only control what one does with their capital, not what the rest of the investment world decides to do with its own. Over time, the quality of the decisions an investor makes will lead to outcomes that determine performance. This can be quick or take an extraordinarily long time. There are often periods where asset prices are stagnant for many years, and then in a month, they have tremendous moves. In these cases, the underlying tactics a company employs over many years show results. The challenge for investors is when the result does not happen in a period that is consistent with what is communicated. If one’s strategy and tactics are correct, at some point, the results prove it over time. With the year ending, now is a good time to review the last year and prepare for the next one. Is the underlying strategy sound? Do the tactics used by each company make sense? What has worked well? Where are the challenges and opportunities for improvement? These are the specific questions I will be considering regarding the assets in our portfolios. It is like coaching hoops, with the analytical piece critical to success.

Spanning the Globe: World Trying to Broker a Ukraine Deal, Bank of Japan Moving to Raise Rates, the UK Loses the Plot, and the 3 Cs Might Bode Well for Free Markets in South America.

The world is focused on the possibility of bringing the Russia-Ukraine war to an end. Ongoing negotiations about the specific terms remain in flux as the US government tries to broker a deal. In Asia, the Bank of Japan appears ready to raise interest rates in 2026. The ten-year Japanese Government bond (JGB) currently sits at a yield of 1.69% with the benchmark rate at .50%. You will notice these are lower than US yields of comparable length. The Yen has long been the borrowing currency where investors borrow in Yen because of the low rates and then invest elsewhere with higher rates. The potential weakness in the investment is the exchange rate fluctuation between what one borrows in and what one invests in. With yields increasing in Japan, the trade becomes more expensive, and the hurdle rate for investment rises. With billions or more funded this way, it is important for investors to pay attention to the specifics, as it can affect liquidity all over the world.

In the UK, the Starmer government has proposals to raise taxes in any number of ways, including higher rates on dividends, potentially taxing electric vehicles, and looking at taxing retirement plan contributions. All of this is related to trying to ‘balance’ a spending program, which is the real issue. What is the famous refrain about socialism?

Turning to South America, the three C countries in the region, Colombia, Chile, and Cuba are all interesting in their own respect, but in combination, the trio reveals what could be an especially important development for the world and investors. Chile may elect a conservative as its next president in the runoff elections scheduled for December 14. Columbia will hold their next presidential election in May of 2026, and like Chile, there is a good possibility of a similar result.

The big development in the region is the escalation of rhetoric between Venezuela and the United States. Venezuela has weakened dramatically in every area under the lack of leadership of its President, Nicolas Maduro, but especially economically. Some political analysts believe Venezuela could eventually change its president with the help of the United States, either economically or through force. Cuba receives much of its funding from Venezuela, so any change in the latter will have large implications for the former. Great, you say, but what about an investment that might benefit from all this?

I have long known about the largest litigation finance company in the United States. It currently trades as cheaply as it has in many years. It has a large judgment pending regarding a settlement with the Argentine government, which has been tied up on appeal for a long time. Litigation finance is the domain of class action attorneys who fund cases and earn the rewards when the cases either settle, or they receive favorable verdicts. The cash flow dynamics of the business are difficult because the working capital cycle can be, uh, ahem, lengthy. I would not expect any returns for a while as the Argentina case has more appeals left and could still take many years for an outcome. Still, the risk-reward is interesting. I’ll send you the bill later.

Y H & C Investments Firm Update- Deal Impacts, and Adding to Existing Positions

November was an interesting month across all areas of the portfolio. In energy, a massive integrated energy company reported solid numbers and progress on monetizing non-core holdings. With a new Chairperson and activist pressure, the market is starting to recognize the improvements at a company with world-class assets. The last year has seen massive successes in new discoveries, especially a large one off the coast of Brazil. It is also helpful when the company generates 40-50 billion in cash and can buy back three billion dollars a year of stock. In other holdings, GE’s health care spinoff bought a medical diagnostic company at a high valuation. In doing so, investors decided to re-price the whole sector, and that helps the valuation of our position. Over the last year, quick-service restaurant stocks have been taken to the woodshed as market leaders suffer from the perception that the consumer is struggling. As such, it presents an opportunity for those investors who are willing to look at what is available. We have built a position in a company that announced it hired an investment bank to consider strategic alternatives. Exciting, eh? Naturally, investors reacted, but this will play out over time as the largest shareholder is the founder, who owns fifteen percent of the stock.

In the small and microcap area, many companies have sold off as this is the time of year when tax loss selling dominates. Quite a few acquisitions have been announced, and with lower interest rates highly probable for the near future, the deal environment should stay strong. With respect to our holdings, as previously mentioned, the deal for the out of home advertising hardware and software provider closed as expected. A little holding in the payment processing space acquired a small entity to help diversify the product range. The one problem is what we often see in micro-caps, and that is questionable capital allocation. Use the stock for a deal when it is at the low end of your five-year price range? Ugh. Another of our positions has been beaten up badly, and I continue to add to this on any weakness. The next month will see the same kind of climate so having an eye out for what you want to own is typically a worthwhile strategy.

Interactive Advisors GARP Models

In the Long Term GARP Model, the buyout of a smaller company was finalized. It was the spinoff of a larger holding and bounced after suffering from a big draw-down. The proceeds were recycled into an existing position in a real estate investment trust. Guess what? The REIT received an offer from the founder and the largest investor to take it private. I added to this after the buyout announcement because there is still a discount to the announced deal price. The company formed a committee to evaluate the buyout offer, but usually, these deals are negotiated before they are announced. A spinoff of the world’s largest ice cream entity by our consumer-packaged holding will take place on December 8.

In the Long Term GARP Concentrated model, we hold the same REIT, so everything said for the GARP model is applicable.

For more information on the models-

Y H & C Investments: Concentrated GARP Investment Portfolio - Interactive Advisors

Y H & C Investments: Long Term GARP Investment Portfolio - Interactive Advisors

I hope you had a great Thanksgiving and t

Thank you for reading the December update. I really appreciate it. if you have any investment questions, please reach out to me at information@y-hc.com.

(Y H & C Investments may have positions in companies mentioned in this newsletter. Nothing in the newsletter should be taken as an offer to buy or sell individual securities. It is the responsibility of each investor to research the investments mentioned so it meets the return objectives, risk profile, liquidity needs, tax circumstances, and specific issues pertinent to the individual.

.png)