.png)

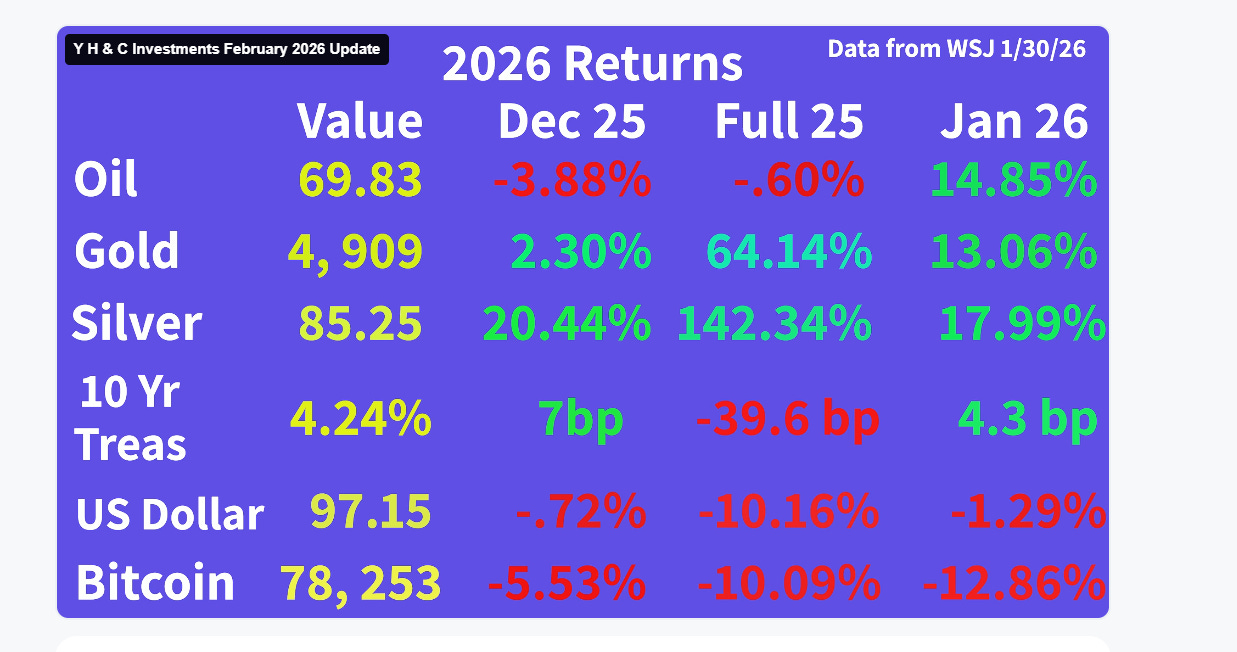

(Return figures come from the January 30, 2026, edition of the Wall St. Journal. Y H & C Investments may have positions in companies mentioned in this newsletter. Nothing in the newsletter should be taken as an offer to buy or sell individual securities. It is the responsibility of each investor to research the investments mentioned so they can decide on the appropriateness and suitability of the investments consistent with their risk tolerance, risk constraints, and return objectives.)

Leaders are paid a lot of money for success. In sports, it is winning games. In politics, accomplishment is getting elected and staying in office. Business excellence is defined by revenue and profit growth over time. A priority is how to make these results happen. In sports, great coaches are consistently able to find ways to get the most out of their people. Today, the best example is the leader of the New England Patriots, who are now in the Super Bowl. The current head coach, Mike Vrabel, inherited a team fresh off a pair of four-win, thirteen-loss seasons. It is why he was hired. The Patriots finished with a record of fourteen wins and three losses this year. Turnarounds happen in the NFL, but often a terrible franchise stays bad for a long time. Look at my hometown Las Vegas Raiders, or the Tennessee Titans, as prime examples. Other examples of dramatic turnarounds include the San Francisco 49ers going from a 6-10 team to a 13-3 season and a Super Bowl appearance under Jim Harbaugh, and this year, the change in fortunes of the Chicago Bears, led by Ben Johnson (going 11-6 in 2025 versus a 5-win, 12-loss season in 2024).

Top coaches do a superior job of putting players in positions to highlight their strengths and hide their weaknesses. In basketball and football, excellent tacticians create situations where the team’s top players get the ball when they have an advantage over those defending them. It is maximizing what your personnel. In baseball, when a manager knows an exceptionally good hitter is up in an important situation, walking them to avoid giving up a big hit is an example of minimizing your potential weakness. These in-game decisions make the difference in each game, and over the course of a long season, add up when evaluating the final record. Why is this pertinent to investing?

As a decision maker, you factor in the capability of management to place capital with those with whom you have the highest degree of confidence. Part of the decision involves the choice of the industry and the position of the company within the competitive landscape. As every company has a balance sheet, there are three parts: assets, liabilities, and shareholder equity. For our purposes, let’s concentrate on the first two. High-quality management teams maximize the value of existing assets and are always looking for ways to efficiently add to a company’s collection. Just as importantly, the assets are organized in a way that makes them efficient to operate and maintain. For example, a retailer focuses on locations in one city, state, and region and then grows in a logistically efficient way to systematically expand in a logical progression. An accurate term given for this effort is asset optimization.

The second piece of the balance sheet is the liability component. It is what a company owes to creditors. They may be short-term, long-term, or based on a future event. It can take the form of accounts payable, loans, bonds, taxes, pension obligations, lawsuit obligations, product warranties, or guarantees. As a company grows, two areas many focus on are tax efficiency and working capital management. Both are related to when cash comes in and when it must be used.

Share Y H & C Investments Weekly Blog & Monthly Newsletter

Excellent management teams structure liabilities in a way that obligations are thoughtfully financed and timed. What you are looking for is low interest rates on debt and having it pushed off as far into the future as possible. The term that best describes this is liability minimization (management). Ideally, there is plenty of flexibility to potentially negotiate debts lower or pay them down with no penalty. Conversely, an enterprise gets into trouble when it assumes too much financial obligation versus the ability and resources to pay. In today’s corporate landscape, creditor-on-creditor violence is a recent trend, where an indebted business pits one creditor against the other to attract better terms on existing liabilities.

Our last section is equity, which can be referred to as shareholder value. As a business becomes profitable, assets are accumulated and used to reinvest and grow more revenue and profit. When a company does an excellent job of acquiring assets efficiently and minimizing the liabilities associated with these assets, equity gets built on a consistent basis and over a prolonged period. It is what investors are paying for when they buy stock. If these elements are in place, there is a chance for success. If not, it is probably not going to happen. Remember, AO+LM= SV.

Spanning the Globe: The US Ousts Maduro and Changes Energy Markets as the Yen Carry Trade Unwinds

On January 3 of 2026, the United States launched a military operation and captured the Venezuelan President Nicolas Maduro, and his wife. In doing so, it has potentially changed the global structure of the energy markets. As Venezuela has the largest proven global reserves of any country, it opens the door for the United States to have long term structural advantage for access, control, and production of hydrocarbon assets, specifically in the western hemisphere. There are definitive challenges to making this a reality.

First, the largest publicly traded energy companies have a history of operations in Venezuela. The only one which operates there today is Chevron. Others left after their assets were expropriated and are owed billions of dollars by the Venezuelan government. Second, the legal status of energy assets within Venezuela places foreign companies in a disadvantaged state in the event there is a dispute. The country changed the constitution this week to make it more open to outside capital. Still, the largest energy entities across the globe have every reason to be cautious about heading back to a country which has a history of being unstable and taking away their valuable assets. Third, any company which is interested in operating in Venezuela is going to have to be prepared to invest a great deal of capital into the infrastructure needed to rebuild the industry. Pipelines, roads, storage terminals, ports, and refineries are all going to need a great deal of repair or investment from scratch to realize the vision of having Venezuela oil production approach a three million per day level. It will not happen soon either. Still, there are many companies interested in the opportunity, so it certainly is worth paying attention to how the situation evolves.

In Japan, the carry trade of borrowing in Yen and investing in higher yielding assets across the globe is beginning to reverse. With leverage of up to fifty to one, currency markets can be the impetus for global selloffs across the globe. There have been many one- or two-day occasions where investors thought the carry trade would reverse, and then it typically calms down.

In Iran, tensions remain high as the US has sent military assets to the Middle East. With reports of Iran slaughtering up to thirty thousand protesters or more, the economic situation in the country remains unsustainable. The planning to try to dislodge an entrenched and barbaric regime is exceedingly difficult in a country of ninety million people. Iran remains a tinderbox and it continues to be the largest opportunity for a different world in many regards.

Y H & C Investments Firm Update- Market Reminders, Beaten Down Sectors, Approval Vote on REIT Buyout, and Small Cap Deals

If ever someone needed a reminder about how treacherous the equity market can be, the largest health insurance company reported earnings last week. It is a four hundred fifty billion dollar a year business. Investors were so impressed with the results that the stock dropped twenty percent in one day, a loss of value of fifty billion dollars. If that were not enough, when the largest software company reported its earnings later in the week, again, investors frowned because of its concentrated pipeline exposure to ChatGPT, and the enterprise lost 350 billion in equity value. Not to be outdone are the loss of value of gold and silver, which dropped respectively over ten percent and thirty percent in one trading day. There are plenty of other examples other reporting companies that are similar. Risk and reward. Not just reward, although to be fair, these examples all have performed very well either over the last decade, or during the recent year and month.

In the event you are courageous, analytical, have patience, and are willing to risk capital, there are obvious areas to look in terms of identifying value. In my mind, the most obvious sectors to consider are payments, REIT’s, media, cable, and energy.

Within our holdings, March 9 is the shareholder vote for the approval of the buyout of our position in the real estate investment trust with properties concentrated in Hawaii. Our position in the small-cap area of currencies reported expected numbers, and the market reacted favorably. A company that I am quite favorable on announced an acquisition that builds on the competitive situation and expands its range of businesses to make the model more durable. It certainly adds an area with plenty of growth potential. Additionally, the fit with the existing portfolio of businesses is tremendous. The deal was financed with nearly all cash, although a very minimal amount of dilution was required for the founder. Leaders have to be able to weigh what is paid versus what is received. In this case, the CEO did very well for shareholders, although that will only be proven in time.

Interactive Advisors GARP Models-

In GARP, our largest position suffered a downgrade and took it on the chin over the last month. It certainly does not help the cause. The position will report earnings in late February. We have quite a few companies scheduled to release results over the next few weeks. In Concentrated, the buyout of our largest position is scheduled to close in the second quarter. Both models hold the REIT with exposure in Hawaii, so what I mentioned above is applicable. The capital will be recycled when the buyout funds settle. The same thing holds true for the buyout of the medical malpractice and workers compensation insurance holding. That deal should close by year end. Again, both models have this position.

For more information on the models-

Y H & C Investments: Concentrated GARP Investment Portfolio - Interactive Advisors

Y H & C Investments: Long Term GARP Investment Portfolio - Interactive Advisors

Thank you for reading the January update. I really appreciate it. if you have any investment questions, please reach out to me at information@y-hc.com.

.png)