.png)

Y H & C Investments July 2026 Update

Take Care of Your House....

Jun 30, 2026

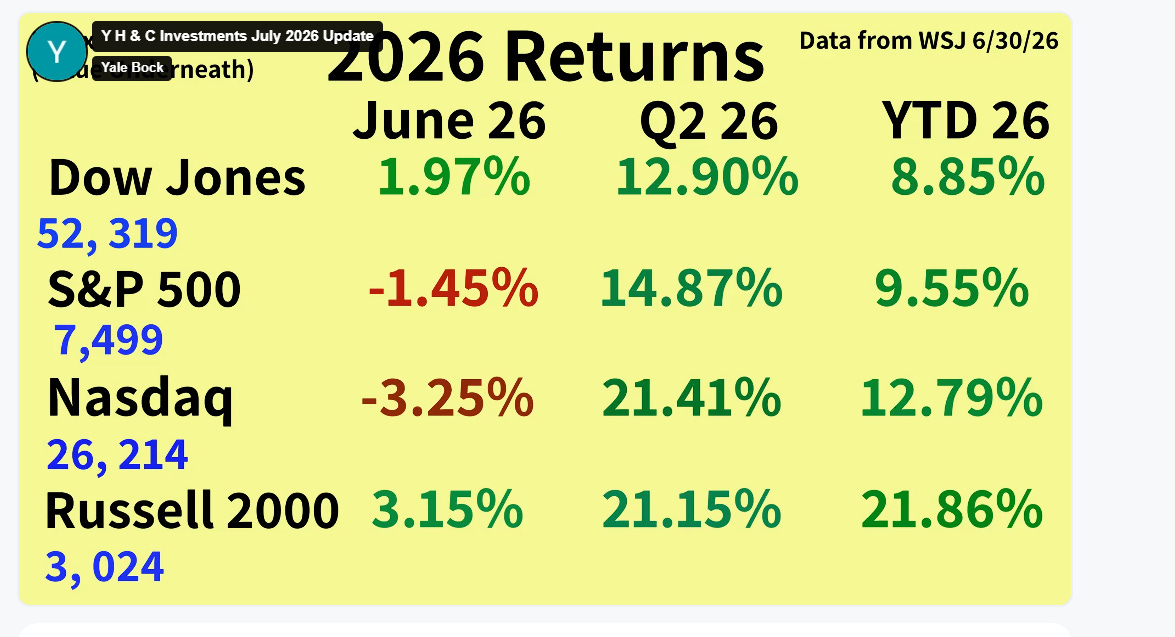

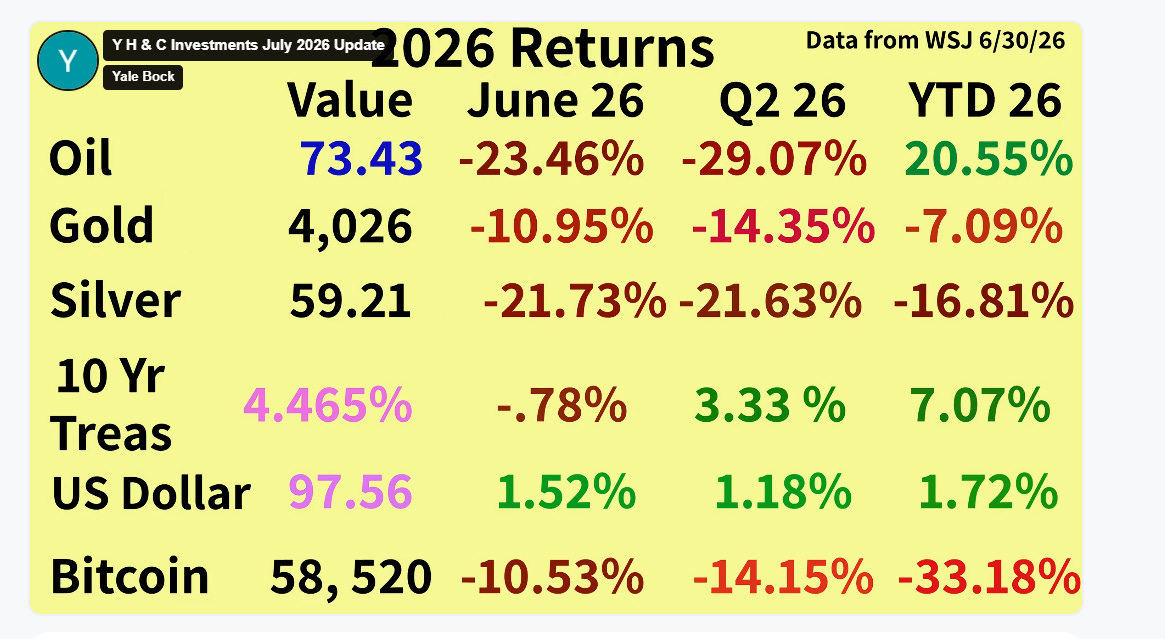

(Return figures come from the June 30, 2026, edition of the Wall St. Journal. Y H & C Investments may have positions in companies mentioned in this newsletter. Nothing in the newsletter should be taken as an offer to buy or sell individual securities. It is the responsibility of each investor to research the investments mentioned so they can decide on the appropriateness and suitability of the investments consistent with their risk tolerance, risk constraints, and return objectives.)

Many people are fascinated by nice homes. Television programs and covers of architectural and better living magazines are adorned with videos and photos of all kinds of stunning places where people reside. If you are a guest at one of these incredible residences, as you enter, the reaction is often an astonishing gasp as you witness a living space where people obviously care deeply about the environment in which they conduct their daily affairs. Often, a fabulous house is adorned with unique art and artifacts, which are colorful and interesting to view. It is spotless, with great care given to the alignment and symmetry of the furniture. You don’t have to be Elon Musk to understand most people would prefer to live in a nice place. So how does this pertain to the investment world?

When you invest in a security, you own a piece of paper (now a digital representative of that paper). It is typically in either the form of debt or equity. There is a precise amount that is created (underwritten) at the beginning of the enterprise. As a company grows, more capital can be raised, and more equity is potentially issued. By issuing more stock, the existing shareholders will not own as much of the company as they did before the new underwriting (issuance). Conversely, if a company buys back stock that is available to the public, existing owners will own more of the company. The best example of this would be a high-profile advertising company that starts with the letter A (it used to be a G). For the last five years or more, it has been buying back stock and reducing the number of shares outstanding. In the last few weeks, it has been announced it would issue more stock, probably because the stock has recently gone up a great deal. Let’s look at a few examples to highlight my point.

Here is an example of the progression of the number of shares outstanding of a microcap company over the last seven years-

160.9 159.5 139.9 122.2 116.9 93.5 7.1 5.80 .1

They went from 100K to 160.9 million. Revenues went from 1.4 million down to 1.1 million. There are no profits anywhere to be found.

Now, let’s look at a different microcap company over the same seven years-

11.3 11.3 11.6 11.9 12.3 12.7 13.0 13.9 14.5 14.5

The number of shares outstanding has been reduced from 14.5 million to 11.3, which is a 22% reduction, or about 3% per year. Revenues have grown from 16.5 million to 33 million, but with a recent acquisition (with 250k shares of additional dilution), revenues will approach 75 million with earnings of over 15 million per year.

The difference between the two examples, both currently listed companies, is dramatic. One treats its existing equity like toilet paper, essentially turning it into something of no value. The other places the highest priority on it’s equity as something to treasure, build, and grow into a valuable asset. Make no mistake, growing the earning power of the business is the number one priority for most companies, listed or not. Still, how the equity is treated by its owners is a crucial aspect of investing. Turning back to our example of houses, one could make the analogy that the industry and competitive position of the company an investor chooses is like the state, city, and neighborhood where you select a house. In real estate, three things matter. All start with the letter l. It is similar in investing, but how the equity is cared for, no matter what size of company we are referencing, plays a critical role in determining the kind of returns investors ultimately realize.

A crucial point for investors is how to think about deal structures during mergers and acquisitions. The pertinent question is what we are getting versus what we are paying, and you must consider how we are paying. Top-quality management teams issue stock for mergers or acquisitions when their own stock is at a high price relative to what they are acquiring. Using all cash, if possible, is always a good alternative because there is no dilution for existing shareholders. In the prior example, the company had cash on the balance sheet because it is profitable and cash built up over time. It used its own cash, borrowed some money by issuing debt, and issued a little bit of stock. In combination, the result is good, provided the company they are acquiring continues to grow its revenues and profits. What you often see are deals where an acquirer is paying too much for a purchase, financed by stock which is not valued highly, resulting in plenty of dilution, and buying an asset which turns out to be a stagnant or declining business. Not good.

Like selecting a house to buy, you want a good neighborhood, meaning an attractive industry. You want the best house in it, or the top company relative to the competition. Above all, you want a management team and board of directors who treat their equity with the highest priority, with great care in building its worth.

Spanning the Globe: The World Cup Arrives

Global citizens are currently captivated by the sporting event known as the World Cup, a once-in-four-years soccer tournament hosted by FIFA. Over 200 countries go through regional qualifying to earn the right to be among the final 48 contestants. Millions of people have traveled to North America to watch the games and enjoy the different cities across the continent. Historically, countries in South America have performed very well during this tournament, often winning it. Similarly, it is currently a region that needs to be considered for investment exposure in the future. Let’s take a quick look, shall we?

If we start with the reasons for investing, the most obvious are the large populations, abundance of natural resources, and the geographical advantages of being located very close to North America in the Western Hemisphere, and still able to export to other large continents like Africa, Europe, and Asia. The most notable challenges include political instability, questions about the legitimacy of the rule of law, volatile currencies, very low levels of per capita earnings power of citizens, elevated levels of poverty, and educational systems that don’t rank highly on a global scale.

The most obvious countries for investment are Brazil, Mexico, Argentina, and Chile. The former two have long been areas with great potential, but ultimately, their investment performance has been underwhelming. Consider this quote by Stefan Zweig (1941), who wrote: “Brazil, the country of the future… and always will be.” Brazil will hold national elections in October. Mexico has long been a socialist stronghold where the country suffers from problems with the rule of law and misallocation of resources, along with a poorly performing educational system.

The latter two countries are the most prominent examples of countries with potential for investment outperformance. A commitment to free markets, rule of law, deregulation, currency stability, and taking advantage of the vast natural resources in oil, gas, and copper makes them areas to strongly consider. With the recent change in political leadership in Colombia, it is also a country that should be looked at more closely. Here is a link to an article which discusses the countries even further-https://seekingalpha.com/article/4874300-from-reform-to-re-rating-south-america-emerging-investment-opportunity

A couple of other interesting tidbits globally include the multi-year weakness of the Japanese Yen and the growing efforts by the non- Iranian countries surrounding the Strait of Hormuz to find ways to ship products bypassing the Iranian side of the passage. The yen currently trades at a decade low against most major currencies and now resides at over 160 to the dollar. It is also only natural to think the neighbors of Iran are more than a little bit fed up with a country that does everything to create bedlam and take advantage of whatever perceived strength they possess.

Y H & C Investments Firm Update- Deal Closing, New Possibilities, Market Sentiment, and Planet Microcap 2026-

June was a busy month across the portfolio as two deals closed and our clients benefited from the realized buyouts. I subsequently reinvested the capital into situations that generate income and are positioned to grow in the future. A holding which we have owned for many years announced a proposed deal to take private one of the two largest gaming companies here in Las Vegas. It is the largest shareholder, and the target owns half of the hotel rooms across the city. At the very least, our company has a blocking position in the event any other entity wants to come in as an alternative. Along with the announced deal for Caesars Palace by Tillman Fertitta, Las Vegas is always a focal point for the investment world.

Markets have been digesting the on-again, off-again pattern of a potential peace agreement in the Middle East, along with wrestling with the enormous spending on semiconductor chips and infrastructure for data centers versus the potential returns on that spending. Return on capital becomes much harder when you are dealing with massive sums like hundreds of billions or trillions of dollars. My take is to let others engage in that handicapping.

My attention is focused on areas I am familiar with and already know, especially financial services, real estate, and payment processing, to name a few. In the microcap area, I attended the Planet Microcap conference held at the Bellagio this month. Like the fabulously run LD Micro event, Planet Microcap does a good job for all attendees and participants. My focus was on the companies that we already have and hearing from the management teams about their current outlook. In this regard, the competitive advantages of why we invested remain or are expanding, and there is plenty of reason to be optimistic about their businesses. I also spent plenty of time learning about new possibilities to put on my radar. It is always advisable to know a wide range of situations where something may be cooking that changes the course of a business’s trajectory. Often it involves new leadership.

July will see earnings reports begin to roll in during the second week, starting with the large banks. I will take a few weeks’ vacation to recharge my batteries, but as always, I am paying attention to the financial markets, and I am sure you are as well.

Share Y H & C Investments Weekly Blog & Monthly Newsletter

Interactive Advisors GARP Models-

In June, the Concentrated GARP model performed nicely with the two buyouts completed. I reallocated the capital into a new position, which helped finance the buyout of one of the acquired companies, along with an existing financial and real estate holding.

In Long Term GARP, it was another challenging thirty days. The buyouts of the existing positions allowed us to redeploy capital into other companies in the portfolio, including the largest financial entity, which continues to suffer from sales in the software area. In this regard, like always, what matters is the quality of

what you are swinging at, and how big are you swinging?

Thank you for reading the July update. I really appreciate it. If you have any investment questions, please reach out to me at information@y-hc.com.

Share Y H & C Investments Weekly Blog & Monthly Newsletter

.png)