.png)

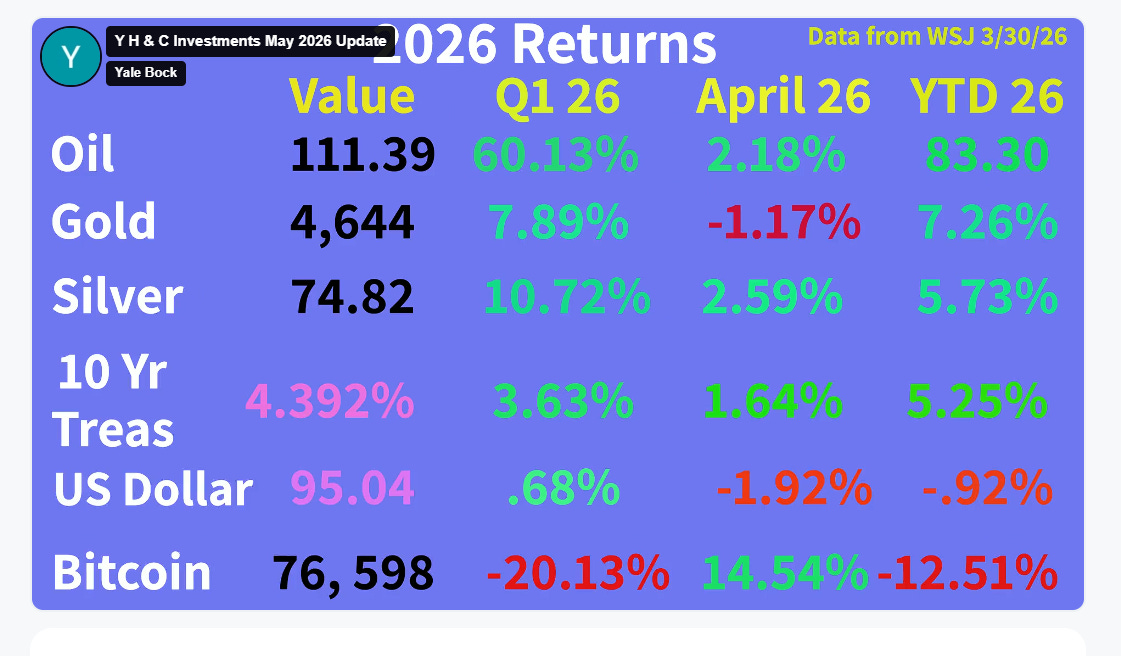

(Return figures come from the April 30, 2026, edition of the Wall St. Journal. Y H & C Investments may have positions in companies mentioned in this newsletter. Nothing in the newsletter should be taken as an offer to buy or sell individual securities. It is the responsibility of each investor to research the investments mentioned so they can decide on the appropriateness and suitability of the investments consistent with their risk tolerance, risk constraints, and return objectives.)

I enjoy golf and used to play a great deal. I was never able to become very good because I just couldn’t master the fundamentals. I really enjoyed the tactical and strategic parts of how to plan out where you should hit the ball, and trying to avoid trouble. The reality of golf for me was that I could understand what to do, but if you cannot execute the shots, it doesn’t really matter. Still, thinking about whether to hit a draw, a low cut, a high fade, trying to stay underneath the hole, all of these little factors that make a difference, I think, is what attracts many people to golf. Also, being outdoors and among some of the most scenic spots in the world, well, it can be quite addictive, especially if you can hit the golf ball flush. Nothing like that feeling, nothing. That is all well and good, but how does it relate to investing?

The advice from Jack Nicklaus on being a champion sums it up quite nicely. You have to understand yourself and what you are trying to accomplish. With the digitization of financial markets, an investor can choose any strategy, tactic, instrument, time horizon, asset class, and leverage amount they want. You can use an artificial intelligence program to set up any criteria you want and compare all kinds of situations based on whatever you are looking for. You can invest in any country, currency, cryptocurrency, option, swap, interest rate, future, or forward, and now use prediction markets on an event basis. Say you are long a stock but think a company is going to miss the quarter. You can hedge your own exposure just by owning a prediction to reflect your skepticism. The world will continue to be your oyster if you are an investor, as the possibilities only grow by the day.

Let’s go back to Jack, my friends. You have to understand your strengths and weaknesses. In my practice as an advisor, I have found it mandatory to have an investment policy statement that outlines the situation, what you are trying to accomplish, and why. As an advisor, I believe you become a better investor because you have to invest based on what clients want to accomplish, so finding the correct fit for asset selection is paramount. Another part of success is understanding that you cannot own everything. You only have so much capital. You can borrow to invest, but then you are introducing time and potentially market pressure if things go against you. You can look at thousands of instruments, and that does not mean you will have success. It means you are spending a lot of time working on finding a good investment, but if that is all investing were about, why do so few professionals manage to outperform indexes over a long-term time frame?

My approach is to be single-minded in buying high-quality businesses and have them work towards becoming larger over a long period of time. Why do I want to own this particular enterprise? Why is this company and management team a group I want to be a minority investor of and partner with? What are the existing competitive advantages, and are they just beginning, potentially getting stronger, or can they be built on? Does the capital structure favor me as an owner? What is the margin and profitability profile of the industry and company? Is the balance sheet comprised of unique assets or liabilities that cause or alleviate financial pressure? Do I understand the current cap table and who influences what the board might be thinking about the future of the business? These are just some of the questions that I take into consideration when evaluating an investment opportunity.

You will notice none of this involves putting any trading limits on positions. I often see other investors say that if a position goes against them by x percent, they reevaluate it. If that works for them, great. It is never even a factor for me. In fact, I believe the biggest mistake an investor can make is selling at the bottom. If ever there was a great example of this, consider the following piece of information from the April 26, 2026, William D. Cohan column in Puck. It sums up how much money Sam Bankman-Fried would have returned to investors if FTX had not been forced into bankruptcy and John J. Ray III had not sold his portfolio of investments. In total, the unrealized gains would be worth an estimated $114 billion. Sam certainly wasn’t ethical, nor stupid, but this highlights the point- you do not sell because you have paper losses, and you certainly do not sell at or near the bottom or a historical price range. In this astronomical example, 114 b’s is a lot of value to forego because of forced selling.

In sum, for me, it always starts and ends with: Is this a business I want to own a piece of? I am not worried about what others own, what they buy, when they sell, what they sell, why they sell, or what they think about the market. By the way, Nicklaus still might be considered the best golfer of all time, so keep that in mind.

Spanning the Globe: The Iran Situation, NATO and the US, and the Western Hemisphere

Share Y H & C Investments Weekly Blog & Monthly Newsletter

The United States and Iran are currently at an impasse with respect to the conditions each country is willing to accept for the Persian realm. There are major disagreements over Iran’s ownership, possession, and use of nuclear material, the control of the international waterways of the Strait of Hormuz, and the funding of satellite organizations that are responsible for terrorism across the globe, especially in the Middle East. No less important are Iran’s appalling treatment of its own citizens and neighbors in the region. The important question is, how will they be resolved? Will it be through negotiation, or with a resumption of military activity? From an economic perspective, the primary issue is what happens in the Strait of Hormuz? If you are a Gulf country that relies on the production and export of gas and oil-based products, the public comments of these entities are that it is unacceptable for them to have to pay a unit toll to Iran on shipments. From a long-term perspective, that will not work for the U.S. and its allies. It is already apparent that the non-Iranian Gulf countries are looking for alternative shipping routes for energy-related products in the future. The countries of Europe and Asia know this is a more important issue for them because they receive a large percentage of their energy supplies from this region. The toll issue is more pertinent to them than a resource-rich country like the United States. Countries in Europe and Asia are making plans about how to handle the Strait of Hormuz issue, but their willingness to accept economic extortion by Iran is probably very minimal as well. Look for the world to find a way to get Iran to back off on this critical issue.

The United States relationship with the countries in Europe, and specifically those of the North Atlantic Treaty Organization, is under severe pressure as a result of the lack of cooperation by the major Western European allies during the Iranian conflict. Repeatedly, a minimal request to allow a fellow NATO ally to use airspace to fly through was denied to the United States. As a result, the current US administration rightly asks what the point of being a member of an organization that is supposed to support one another is when, historically, the easiest and most straightforward actions are denied. This has heightened importance during the course of a major military event, which involves the United States at war with a country that is actively seeking to use ballistic missiles against NATO countries. It is hard to see a future where the United States is part of this alliance.

Turning to the Western Hemisphere, it is very apparent that the current US administration views anything close to home as off-limits to foreign adversaries. The most obvious potential problem is the deep connection and financial support of China in Brazil, which has accepted billions of dollars of aid and investment in logistically advantaged ports and infrastructure. China needs oil and gas from wherever it can get it, and Brazil’s Petrobras can deliver. Look for this to be a continuing source of conflict both today and in the years ahead. Obviously, US control of oil in Venezuela and the potential for future regime change in Cuba after the Middle East conflict gets settled are major topics to pay attention to as the year progresses.

Y H & C Investments Firm Update- Earnings Season, LD Micro, and Capital Allocation

April was an interesting month as earnings season began a few weeks ago, with the banking segment reporting generally very strong numbers. Our large diagnostic health care position reported the strongest quarter I can ever remember, and it has a great deal of momentum as a critical component across the entire health care landscape. I met with a couple of long-time investors a few weeks ago and remarked that the health care value chain is quite interesting because there is clearly one group of companies that captures the vast majority of the profits. There are other high-quality entities in the massive industry, but one group overwhelmingly stands out among them. Our big holding in the largest publicly traded coffee company was rewarded with the best quarter in two years, as the company is starting to gain momentum. A large consumer packaged goods holding reported and entered into a deal where they are merging their food holdings with the largest spice provider to form a massive player in this segment. This will be the second financial engineering transaction this company has engaged in over the past year. Investors would not typically expect a packaged food company to be so active in searching for ways to create value, but creative management teams look at a variety of different ways to benefit shareholders if they are really concerned about creating the ever-elusive shareholder value.

In the middle of May, I will be headed to the LD Micro conference in Los Angeles. Many of our smaller companies are reporting their results over the next few weeks. One issue for many small companies is the constant turnover in the C suite. When the CEO and CFO change every year or every other year, it is very difficult for an investor to place any faith in the organization’s credibility. The biggest challenge for most companies, and this is especially true for small microcaps, is capital allocation. Evaluating deals, lining up different financing alternatives, considering whether to invest in organic growth and which part of the business to allocate capital to, and judging the market price of the equity for valuation are the critical skill sets which help determine future growth. In many cases, with equity prices trading at levels that disgust CEO’s, the obvious temptation is to buy back the stock, especially if the company is profitable and has a healthy balance sheet. It needs to be done at a very attractive price and probably over an extended period of time for it to make a difference. The real secret to having an appreciating share price, in my opinion, is top-line growth and expanding margins. Buybacks will reduce the denominator, but if the numerator is not expanding at an impressive rate, especially if you are a small company, investors are not going to reward the result. Yeah, I know, really going out on a limb there, huh?

Investor day is May 1, and this weekend is the Berkshire Hathaway Annual Meeting. Many investors will make the annual pilgrimage to Omaha, but without Munger and Buffett displaying their one-of-a-kind brilliance and spirit, it just is not the same in my mind. Their enduring lessons of behaving with class, thinking for yourself, and being very rigorous about what you want to own are characteristics you don’t have to travel to Omaha every year to employ. I know many value investors who will be there, and I hope they all have a good time and travel safely and conveniently.

Share Y H & C Investments Weekly Blog & Monthly Newsletter

Interactive Advisors GARP Models-

In April, the Concentrated GARP model performed well. This can be attributed to strength across the portfolio, as quite a few of our holdings are buying back stock. A few presented at investor conferences and are actively buying back their equity. Our energy holdings were again strong contributors to the portfolio.

In Long Term GARP, the portfolio increased a little bit, but the biggest headwind remains the continuing perception of the entire software complex. Our large tax and financial services holding remains grouped in with this cohort. The rest of the portfolio has balanced some strength in energy with weakness in anything consumer or health care related. We took the opportunity to trim a high-end discretionary holding and reinvest in legal tech, which has been sold off like the rest of the software group. With the software area selling off as hard as it has been, when high-quality companies are being tossed away, you certainly have to take a hard look (or maybe even more).

For more information on the models-

Y H & C Investments: Concentrated GARP Investment Portfolio - Interactive Advisors

Y H & C Investments: Long Term GARP Investment Portfolio - Interactive Advisors

Thank you for reading the May update. I really appreciate it. if you have any investment questions, please reach out to me at information@y-hc.com.

.png)