.png)

(Return figures come from the August 29, 2025, edition of the Wall St. Journal. Y H & C Investments may have positions in companies mentioned in this newsletter. Nothing in the newsletter should be taken as an offer to buy or sell individual securities. It is the responsibility of each investor to research the investments mentioned so they can decide on the appropriateness and suitability of the investments consistent with their risk tolerance, risk constraints, and return objectives.

“The whole is greater than the sum of its parts.”: – Aristotle.

When one is in their youth, the issue of searching for a companion is often at the top of one’s mind. The libido can take precedence over anything else, especially if there is a certain chemistry that clicks with another person. It is in this spirit that marriages can be the natural progression of this kind of relationship. In combination, both people find more happiness together than they would apart. Naturally, the next step would be to procreate and add a family member to this happy union. We can see that Aristotle did not necessarily refer to personal relationships when he issued his comment about the whole being greater than the parts. How does this apply to investing?

First, companies often seek out other enterprises to become larger, more efficient, more profitable, or improved entities by virtue of adding product lines, intellectual capital, additional assets, or some combination thereof. Second, one tactic of investment is to identify companies where there is a large quantity of assets or operating businesses that the investment community is not recognizing for their total worth. The term given to this style is the sum of the parts investing. Now, let’s consider what is taking place in the world, which has many investors agog over the possibilities. It is the tokenization of every asset that can be sliced and diced.

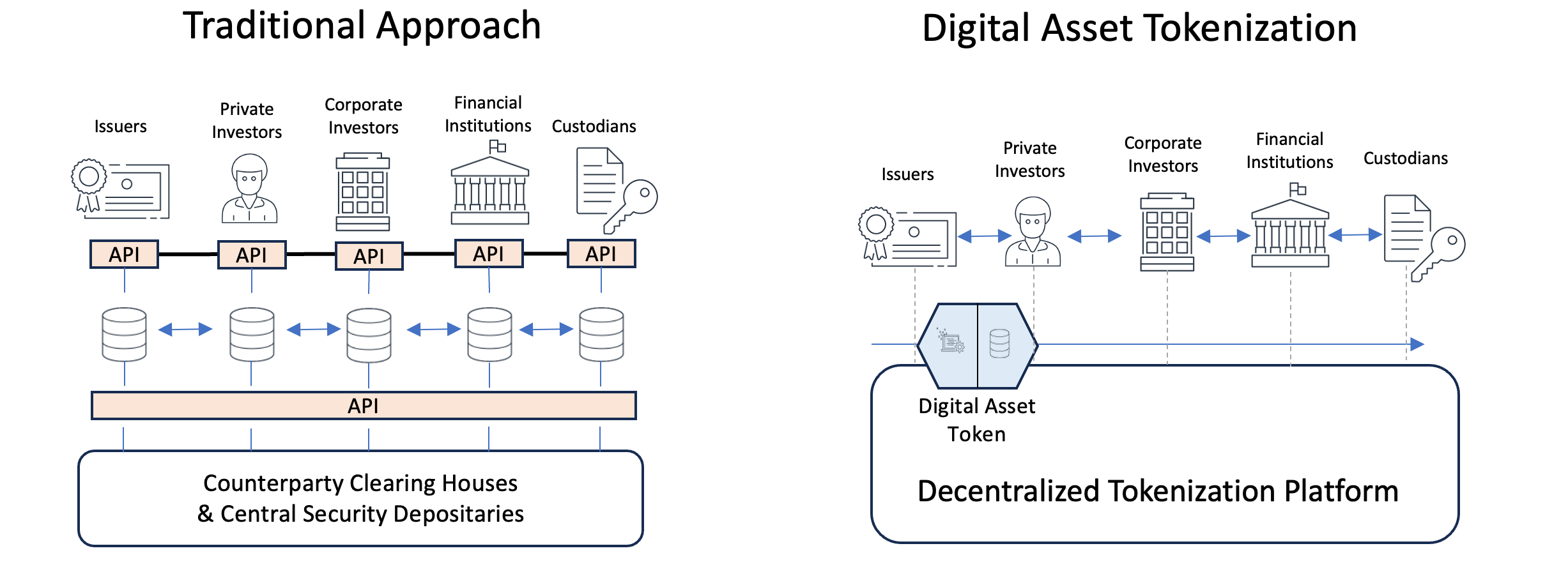

What exactly is tokenization? Tokenization is the process of converting the ownership rights of any asset into a digital token on a blockchain. The concept of “tokenization of everything” is accelerating as institutions and investors digitize a vast array of assets, from real estate to stocks.

The underlying principle involves using smart contracts on a blockchain to create and manage these digital representations. Each token contains the rules and rights of ownership for the asset it represents. The range of assets that can be tokenized is comprehensive, encompassing financial assets, real estate, intangible assets (intellectual property- including patents, music royalties, carbon credits, and renewable energy), collectibles, and currencies. Proponents argue that the benefits of tokenization are improved liquidity with fractional ownership, which can be subdivided as small as one can imagine, and improved transparency with every record on the blockchain. All payments, like dividends, are automated for faster settlement and lower minimum investments, providing much wider access to previously restricted assets.

The move to digitize everything allows banks, brokers, and custodians to offer every kind of transaction possibility in one place. You are seeing it happen at Fidelity, Schwab, Chase, BlackRock, Blackstone, and many others, giving access to digital assets like crypto-related tokens and stablecoins, along with stocks, bonds, cash, indexes, CDs, and in retirement accounts. From my perspective, a key issue is reducing costs and settlement times for those responsible for custody. From an investment point of view, just because an asset is tokenized and made more accessible does not make it more valuable. More people may be able to buy it at smaller dollar amounts, but the mere fact that it can be purchased more easily does not make the underlying economic value increase over time. In many cases, more assets are issued each year, which makes the threshold for acceptable levels of growth higher. If you split a pie into more pieces, it does not make the pie taste better or allow the owner to sell more pies. It makes it easier to buy one piece, but if the pie is not delicious and does not look good, people are not going to buy it.

If we take this even further, access to IPO’s, private company assets like venture capital-based startup companies, private credit (loans and debt instruments), secondary debt underwritings, private equity portfolio companies which are not public, futures, forwards, swaps, options, commodity linked instruments, bank accounts, frequent flyer and customer rewards, and who knows what else, are all there for slicing and dicing into monetizable assets. The world is entering the era of tokenization, whether we like it or not. Choosing carefully takes on even greater importance.

Spanning the Globe: Deals with Japan and China, and Milei Surprises in Argentina-

President Trump is in Asia and has announced several economic deals with countries in the region aimed at resolving trade-related issues, including the fairness of tariff rates and access to markets. The most prominent arrangements are with Japan and China, and the critical point of rare earth materials is a big piece of the negotiation. Japan agreed to invest up to $550 billion in US projects that provide rare earth materials and supplies different forms of nuclear material. The rare earth and nuclear components are estimated to be worth up to $400 billion, and the US is finalizing a 15% tariff rate by the US on Japanese car exports. There are all kinds of rumors swirling about US deals with China, which could take place when the two countries meet in South Korea. The investment community is focused on a few important areas. The first is semiconductors, and the effect of tariffs and trade restrictions on large manufacturers. The second is the critical issue of rare earth materials and China’s dominance across the supply chain. These are high-priority areas for both countries and the rest of the world and will be for the foreseeable future. A third is the energy sector, and the most obvious topic is the relationship between China and Russia.

In Argentina, President Milei surpassed expectations in the country’s midterm elections. Helped by a $20 billion swap line established by Treasury Secretary Scott Bessent, Milei’s political results will help him shore up the country’s finances with outside creditors, especially the International Monetary Fund. High borrowing costs and currency weakness continue to plague the country, but both have improved dramatically under Milei’s dramatic move to free market policies. With the large oil and gas deposit of the Vaca Muerta waiting for more infrastructure, outside capital with better funding arrangements and more certainty seems only a matter of time. Politically, the related escalation of tensions between the United States and Venezuela has enormous implications across the globe, but especially in the southern hemisphere. Venezuela has the largest oil reserves in the world, and a change in leadership could make a massive difference in many areas and industries, but especially in South America and the oil and gas sector.

Y H & C Investments Firm Update- Banking and Health Care Results, A Good Deal, and Conference Tidbits

In October, quarterly earnings started streaming in across the corporate landscape. It always starts with the largest banks, which set records across the board. Of note were cautious comments about private credit. The large bankruptcies in the auto sector of First Brands Group and Tricolor Holdings brought the exposure of JP Morgan Chase, UBS, Jeffries, and Fifth Third Bank into focus. Elsewhere, related liability of Zion Bank and Western Alliance has investors wondering where and when more problems might emerge in the credit area. In health care, the largest companies reported strong earnings as well, but the sector has sold off recently. Buy the rumor, sell the news seems to be the well-established routine of investors these days, other than for a few rare companies.

With respect to our positions, a deal for a large energy company is nearing completion. For our clients, we elected to take all stock in the acquiring company versus all cash or half cash and half stock. Receiving all stock is a non-taxable event, whereas anything with cash is a taxable gain. In combination with the acquiring company being US-based and the acquiree from Canada, clients will save foreign withholding taxes on all future dividends, which will now come from an entity twice as large. In the micro-cap space, a position we have held for a few years, announced a deal that will double the size of the company. It is a provider of reader boards and content management software in many areas, specifically for large arenas, retail outlets, and quick service restaurants. It is the classic example of the razor-razor blade business model, in theory, very much like Apple. The combined company will have projected revenues of more than $100 million and help improve cash generation to above double-digit margins. The deal is waiting for regulatory approval in Canada, and that is imminent. When I first met with the company, it was much smaller and at the end of a deal with a similar impact. It is illustrative of what can happen in the micro-cap area over the course of a few years. Large changes are possible, but it takes a very focused management team and plenty of diligence, along with extreme patience by investors. Elsewhere, a company where we have a sizeable position announced a rights plan for existing investors to prevent any kind of corporate takeover.

Recently, I attended both the LD Microcap conference in San Diego and the Planet Microcap Conference in Toronto. Both of the events were top-notch and ran fabulously. The best part is meeting with excellent people, many of whom I already have a relationship with, and some of whom I met for the first time. There were plenty of interesting companies, and a common theme is that all believe their stock is undervalued. Quite a few were extremely disappointed with where their stock traded. In these meetings, I try and learn the story about what makes a company unique. Equally as important is whether I believe in the people who are explaining it. A good frame of reference for comparison is the companies in which we already have positions. Venture capitalists often say the criteria for investing in a new company is that the product must be ten times better or more than the existing competitors. If this is a guideline, new positions must be significantly better companies than those we already own. Another common theme you hear is that in a few years, a company will be ready to sell, but at a much higher price than what the stock trades for today. Shock. All in all, these were good experiences and worthy of my time and effort.

Interactive Advisors GARP Models

In the Long Term GARP Model, the diagnostic health care holding reported record earnings, and the stock sold off. A position in the quick-service restaurant area reported numbers that were dramatically better than expected, and the sentiment going into the report was very low. A similar situation took place with a real estate investment trust position, as it is considered an office REIT even though it has segments in multi-family, retail, and mixed-use hotel and retail.

In the Long Term GARP Concentrated model, a position in the largest cable and wireless entity in Canada, as well as the owner of many one-of-a-kind sports and entertainment assets, reported strong numbers. It is a dominant company with unique businesses that occasionally get cheap. A holding in the telecommunications billing area reported earnings that were in line but not well-received by investors. In this regard, the major league for investors is concentrated around technology and large banks, especially in the semiconductor and artificial intelligence industries. Everything else is ignored and not afforded many looks. Super. More opportunities for those of us who are interested.

For more information on the models-

Y H & C Investments: Concentrated GARP Investment Portfolio - Interactive Advisors

Y H & C Investments: Long Term GARP Investment Portfolio - Interactive Advisors

Thank you for reading the November update. I really appreciate it. Have a safe and happy Halloween, and if you have any investment questions, please reach out to me at information@y-hc.com.

(Y H & C Investments may have positions in companies mentioned in this newsletter. Nothing in the newsletter should be taken as an offer to buy or sell individual securities. It is the responsibility of each investor to research the investments mentioned so they are in alignment with one's return objectives, risk profile, liquidity needs, tax circumnstance, or any other issue pertinent to their personal situation.

.png)