.png)

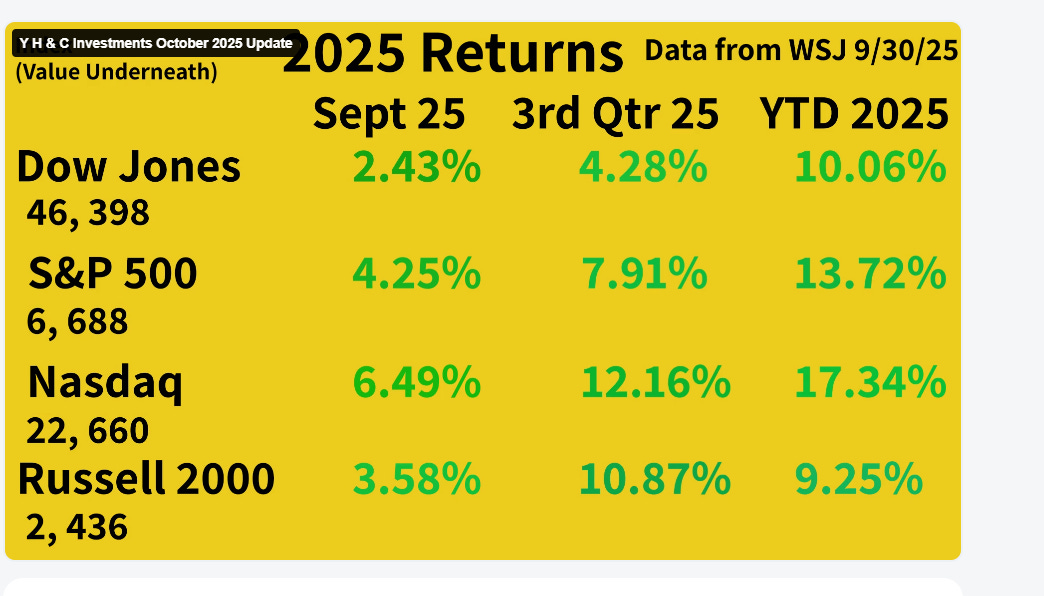

(Return figures come from the August 29, 2025, edition of the Wall St. Journal. Y H & C Investments may have positions in companies mentioned in this newsletter. Nothing in the newsletter should be taken as an offer to buy or sell individual securities. It is the responsibility of each investor to research the investments mentioned so they can decide on the appropriateness and suitability of the investments consistent with their risk tolerance, risk constraints, and return objectives.

When a person is in their youth, let’s call it from sixteen to thirty years old, finding a life partner is of interest, if not a high priority, for many people. There are societies where cultural norms dictate the available universe of potential mates. The approach one takes in finding a potential mate is as diverse as there are humans. Some might place a high priority on physical appearance. Others might place a heavier weighting on friendship and compatibility. Let’s consider two approaches. The first person is a social butterfly who is active in the bar scene. Each weekend, they go with their friends to a local club to have a good time and enjoy the allure of finding their one-in-a-million dreamboat. On occasion, they might drink a few too many beverages and engage in extracurricular activities where they wind up in situations where they don’t quite remember, or are comfortable with, the person they are now faced with, or, um, ahem, even closer.

The second person approaches their social activities differently. They concentrate on attending weekly and monthly religious ceremonies and events. A heightened emphasis is placed on understanding where the potential mate is from, meeting their parents, and spending time learning what makes them happy, sad, indifferent, or excited. A friendship is formed through learning, and a common bond is established over their shared views on various subjects in which they both participate. Clearly, these are distinct approaches to the same problem. We can apply this idea to the current state of affairs in the investment world.

As of August 2025, in US public markets, there are currently approximately 4,300 ETFs (exchange traded funds) as compared to 4,200 publicly traded companies. In terms of recent trends, the number of ETFs grew by approximately 4 per day in 2025, while the available publicly traded companies continued to shrink, losing nearly 500 in 2024 alone, down from 6,500 in 1997. I bring this up because the investment world has been moving to a passive approach for a long time, and the amount of capital allocated to index and ETF-based approaches is now greater than the active methods.

Over the last few decades, the S&P 500 has been the star performer of all indexes. Currently, 35% of the S&P 500 is made up of seven companies. Many other ETFs have a similar dynamic where a few companies constitute a heavy weight within the instrument. Prominent examples include the QQQ, IVV, SPLG, VOO, VGT, and TOPT, not to mention the Ark fund complex. Investors are drawn to the lower risk, ease, and cost of indexes and ETFs and have been rewarded by owning instruments tied to large tech companies, which have grown substantially. The enthusiasm for artificial intelligence over the last few years has led to high-profile recent offerings like ARTY, CHAT, BAI, AGNT, and IVES. Investors who adopt this approach believe what has been working will continue to work. The current valuations of these assets are, let’s be kind, historically elevated. How do I approach the market knowing these facts?

One caveat, I am an active investor, so I am biased, and I am talking my book. ETFs are made up of different assets, but in most or many cases, the holdings are individual public companies. One is a derivative of the other. If you understand derivatives, you know the secondary is a function of the primary. As such, what matters is the performance of the core companies. The ETFs will rise, and fall based on those entities. So, for an active investor, more attention to ETFs is good because less capital is directed toward finding and analyzing individual companies. The number of individually listed enterprises shrinking means the strongest survive. History has proven that Darwinian concepts are applicable in markets as well. It has long been understood that the small and micro-cap areas are the most inefficient areas of the market. Inefficiency is good for active investors because it means mis-pricing. It is also excellent for active investment because if one is accurate about the analysis of a small company, the runway for expansion is much greater than a bigger entity. Conversely, investors who allocate capital into areas where there is more competition and great enthusiasm are placing a great deal of belief in the premise that massive amounts of capital allocation will yield acceptable returns. When large amounts of money are involved, just because it is spent doesn’t mean an above-average return is earned. Look at what Stevie baby spent on the Mets payroll this year, and uh, no playoffs again. In sum, less competition, fewer investors looking, mis-priced assets, large expansion possibilities versus greater numbers of instruments, top-heavy weighted assets, recent outperformance, and elevated valuations. Capital will flow where it is best treated. Markets change, like nearly everything else, though often it takes decades, not years for the difference to become evident. What one chooses is based on their own perceptions, just like choosing an ideal mate. Future returns depend on your selection, so be thoughtful.

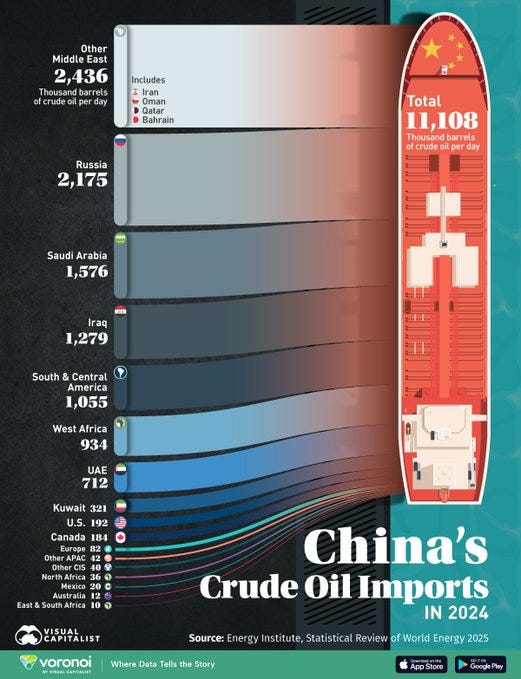

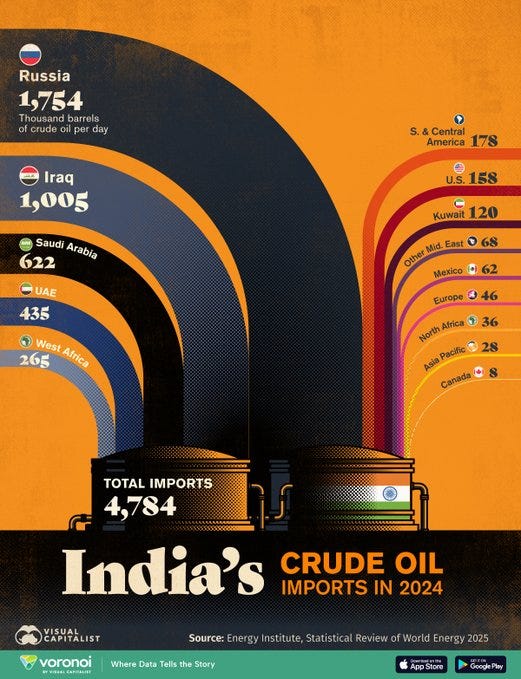

Spanning the Globe: The Impact of China and India on Critical Industries

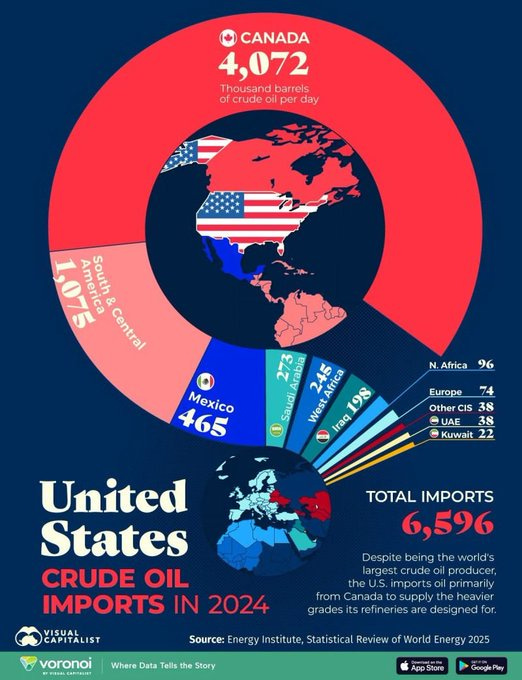

The infographics above give us information about oil consumption from the largest global countries. The ability to produce as much of one’s own energy as possible is a strategic objective, if not a priority. The next best alternative would be to have readily available sources as close as possible to friendly countries. An analysis of the infographic makes it very clear which country is most advantaged.

The two that have distinct disadvantages happen to be the largest countries. As such, their political actions should at least take into consideration their resource situation. Resource availability has a crucial impact on understanding the economics of many industries. The most prominent example is artificial intelligence. Two areas that are crucial to it are semiconductors and energy. The ability to produce semiconductors in high volumes without defects is the primary factor for supplying the brains of computers and servers that run data centers. Semiconductors are also critical to the defense industry for use in precision-guided missiles, which are guided by GPS systems. The companies in Silicon Valley have long adopted the fabless production model, which means the large foundries that make the chips are dominated outside the US, primarily by one company. Recent moves by recent US administrations are trying to change this issue. In fact, the US announced a deal last month to make an equity investment in a prominent US company to help improve domestic semiconductor manufacturing capability.

Tied in with the artificial intelligence topic is the ability to supply the power to the data centers and also cool them. Natural gas, nuclear energy, and water are all the source elements involved with this dynamic. The race to construct data centers across the globe is the headline that has the investment world captivated by the immense backlog of orders of semiconductors. The ability to supply energy to power these massive buildings has energy companies in an excellent position, as natural gas is the primary source that will probably be used. Nuclear energy is seen as potentially an important provider as well. Water and coolant are needed, so those areas have also moved up in current investment perception.

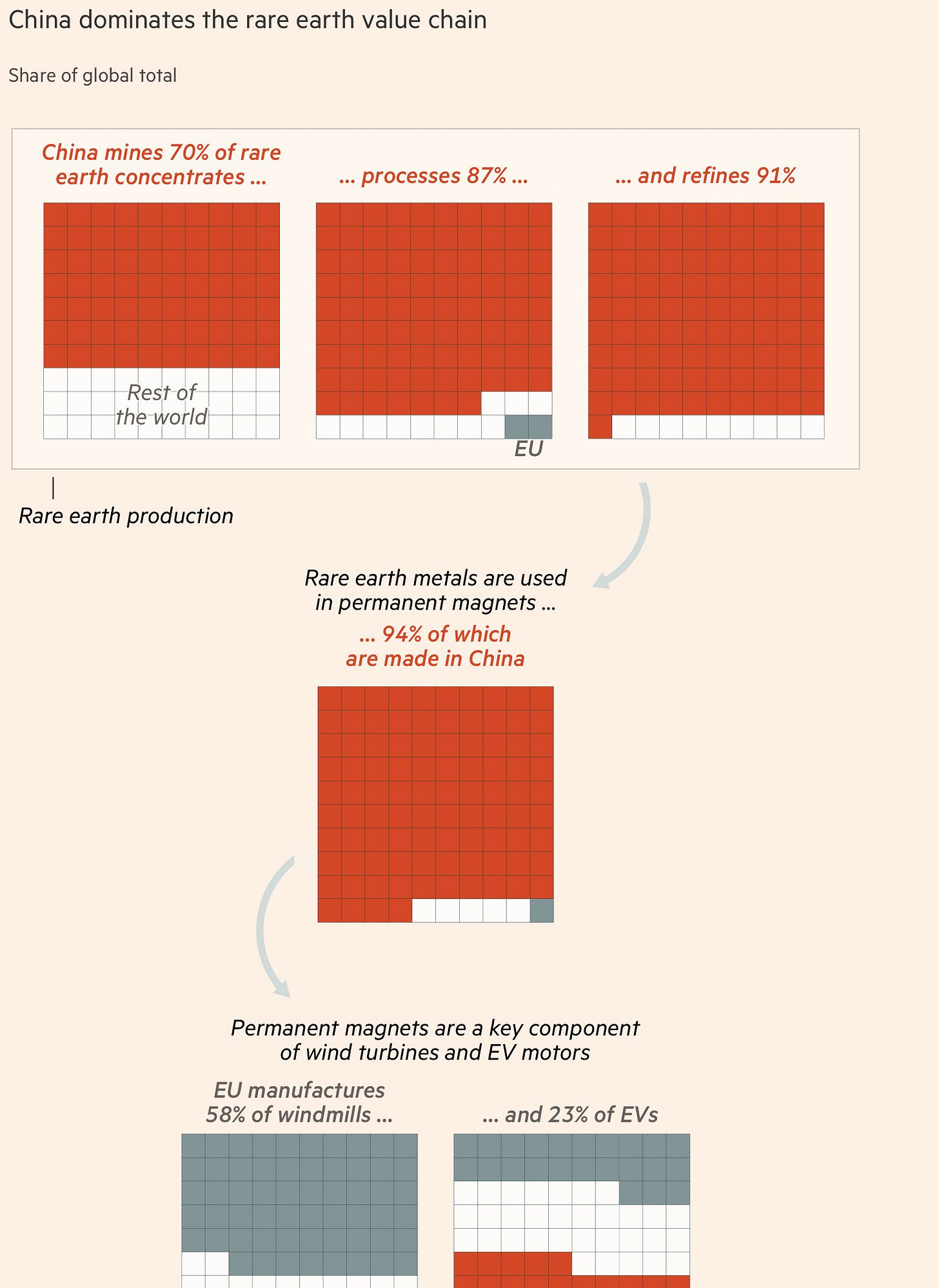

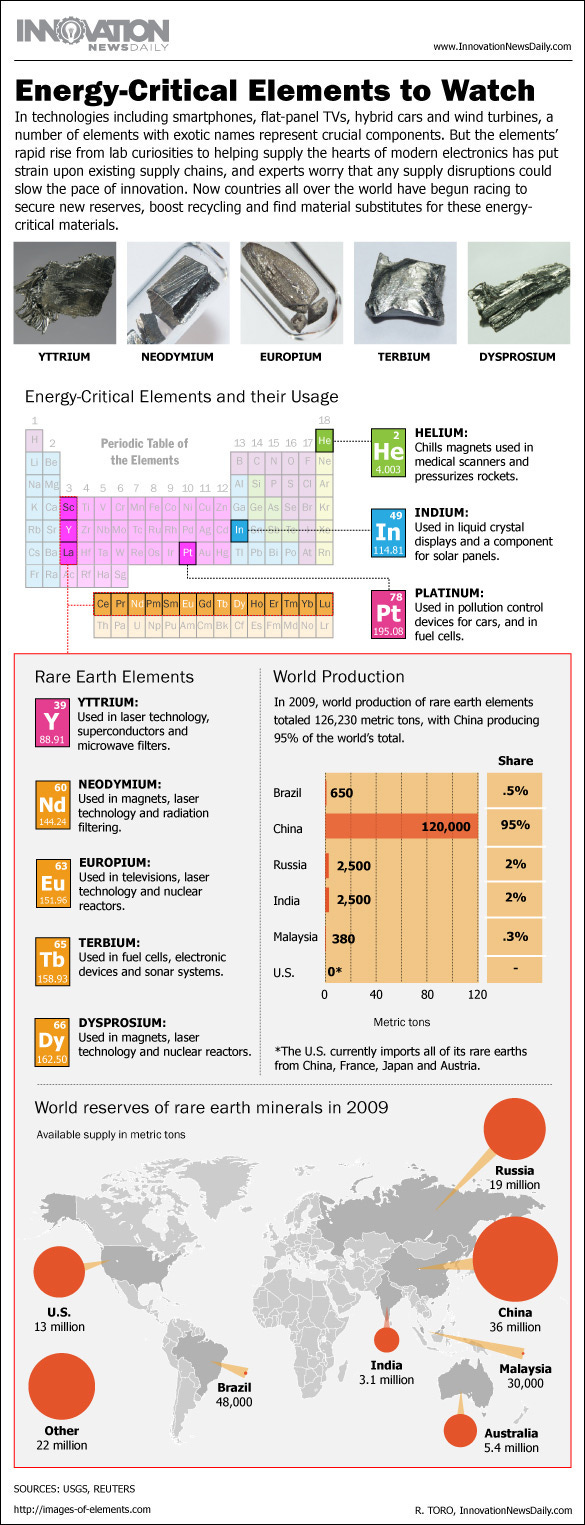

In the defense and transportation area, China is the lead country to watch because of its dominant position in many rare earth materials. These elements are critical to supplying different components across the military and movement complexes.

The situation is clearly one that leaves the United States vulnerable, so the current administration is changing industrial policy to try and improve US competitiveness. Over the last few months, equity investments by the government into companies in different areas have piqued investor interest. Like the semiconductor area, the commonality is that changing the situation takes a long time. Large supply sources need plants to be able to process the raw materials, and the plants take a long time to get locations, funding, permitting, and then to be built. It is a dynamic not helped by dysfunctional governments, which can’t agree on where a bathroom is allowed, let alone who is legally permitted to be in the bathroom. Just look at the imminent US government shutdown as an example. Segments that are drawing enormous attention include rare earths, lithium, copper, steel, tin, helium, neodymium, and others. Makes you want to go back and rethink chemistry class, eh?

Y H & C Investments Firm Update- Monitoring Existing Holdings, Preparing for Conferences, and Lessons from Malone, Dimon, and Diller

September has been an interesting month in the market. Historically, September and October are believed to be the most challenging months for investors. My own experience has been that they often turn out much better than investors expect. Quite a few of our entities were at investment conferences, and we read through the transcripts to monitor their business updates. In our holdings, health care, real estate, and financial entities were beneficiaries. A few unique circumstances regarding takeovers and mergers also helped a couple of positions. We will take it, and as the year moves to the last quarter, we have been fortunate as a few are being bought, merged, or taken private. The lesson we take from this is that identifying the highest quality businesses at prices that make sense will eventually lead to a good result. We have no idea when and in what form. The better the business, the more the odds move in our favor. A key question to evaluate is the existing competitive advantages and their durability. Of equal importance is the quality and incentives of the management. Additionally, what are the reinvestment opportunities for existing profits? Finally, and this is very important with the smaller holdings, where are they in the life cycle of building and creating a unique and advantaged business? Currently, a focus for me is the quick-service restaurant area. Many larger companies are out of favor, just how we like it.

During the month of October, we will be attending two investment conferences on the week of October 19-25. The first is the wonderful LD Conference in San Diego, CA, run by the legendary Chris Lahiji and Scott Biddick. The second is the Planet Microcap conference in Toronto, Canada, with its own legends, Robert Kraft and Ian Cassel. These are the top two investment conferences in the small and microcap area, and I am booked with management teams of all kinds. Many are holdings where we have existing positions. The industries are concentrated around specialty finance, banking, payment processing, real estate, consumer discretionary, and a little bit of energy and raw materials. No mining, crypto, and cannabis for me. I spend the months and weeks leading up to the conferences preparing to learn as much as possible during these important few minutes.

The investment world is a hyper-competitive industry, and without reading and being immersed in it at all times, it is going to be difficult to produce good results. September saw the release of a couple of excellent books from the leaders of high-profile enterprises, which we have been fortunate to benefit from. The first is called Wired, by John Malone, who built TCI Cable and Liberty Media into incredibly successful entities with holdings in many areas. It was interesting to learn his views on businesses and events we only learned about after public information was released. The major lesson for application in the future is to look for problem solvers. Malone excelled in finding ways to unlock value from positions he owned that the market did not find attractive. He also was an incredibly opportunistic buyer of assets others thought had little worth or were beaten down by current investor sentiment. The ability to create value in different ways is a hallmark of a top-notch leader and is very difficult to find.

The second book is Who Knew, by Barry Diller. The lesson to take away from this book is the role of content creation in creating value. It has become much more difficult for content creators as competition is enormous and the barriers to entry are essentially nothing. Still, the approach by Mr. Diller in terms of how he looks at evaluating ideas was fascinating, and his success is unlikely to be duplicated.

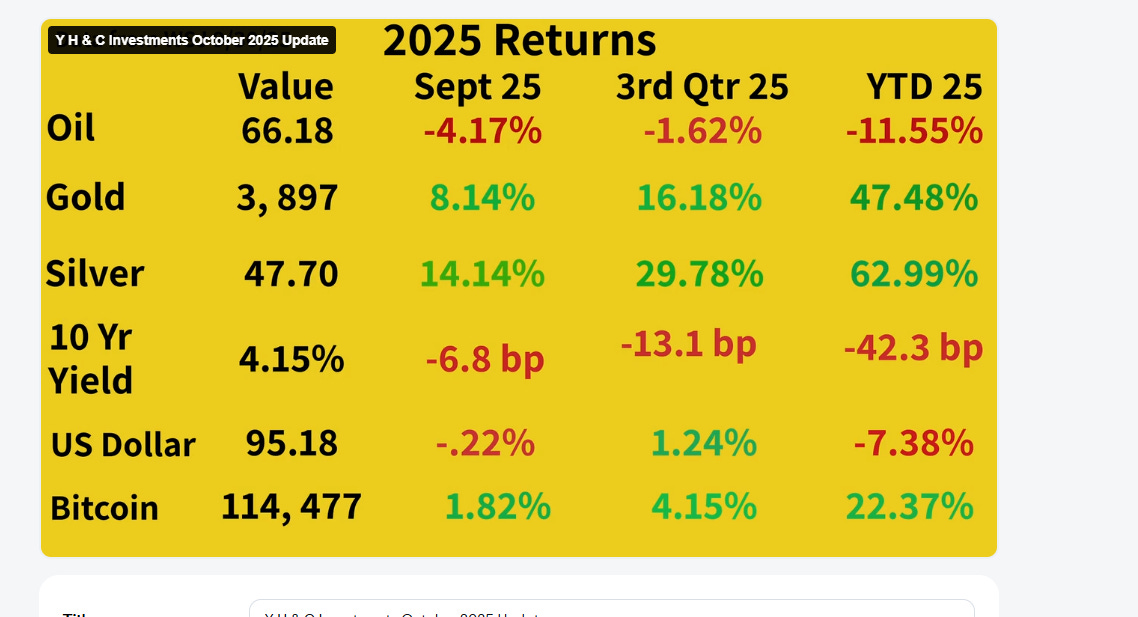

In looking at the current conditions in the market, the Fed just cut interest rates by twenty-five basis points, and it appears there will be two more cuts before the end of the year. GDP growth is estimated to come in at about 2.5-3.0 percent for the year, with the last quarter recently revised higher. Lower interest rates should help housing, banking, and real estate-related industries, and merger and acquisition activity is picking up. Heading into the traditionally strong fourth quarter, one would expect market sentiment will continue to be positive. The fly in the ointment is the fiscal and monetary positions of the US, running 6% or more budget deficits and the ever-growing national debt. Dollar weakness is seen continuing as gold and silver make record highs daily. Finally, another great interview with Jamie Dimon is worth one’s time. These leaders created an immense amount of wealth for shareholders.

Interactive Advisors GARP Models

In the Long Term GARP Model, a few events of note were a smaller holding getting acquired, which is expected to close in the fourth quarter. One of the top two global consumer packaged goods companies is spinning off its ice cream segment into a separate company, and that is expected to occur in December. A real estate holding bought the apartment communities segment from the highest-profile publicly traded homebuilder.

In the Long Term GARP Concentrated model, there is interest from the largest cable and wireless company in Canada in spinning off or taking public its media and sports segment, which includes some of the best sports teams and content in North America. The same real estate holding I mentioned in the GARP model is also held in the Concentrated GARP model, so we will get the benefit of the transaction in this model as well. Finally, with the help of the wonderful Sean Aronson, we added a new simulator to my website for investors to work with in evaluating these models- you might take a look here-

For more information on the models-

Y H & C Investments: Concentrated GARP Investment Portfolio - Interactive Advisors

Y H & C Investments: Long Term GARP Investment Portfolio - Interactive Advisors

Thank you for reading the October update. I really appreciate it. Have a safe and happy October and Halloween, and if you have any investment questions, please reach out to me at information@y-hc.com.

(Y H & C Investments may have positions in companies mentioned in this newsletter. Nothing in the newsletter should be taken as an offer to buy or sell individual securities. It is the responsibility of each investor to research the investments mentioned so they can decide on the appropriateness and suitability of the investments consistent with their risk tolerance, risk constraints, and return objectives)

.png)