.png)

Keep the Alphabet in Mind-

Sep 01, 2025

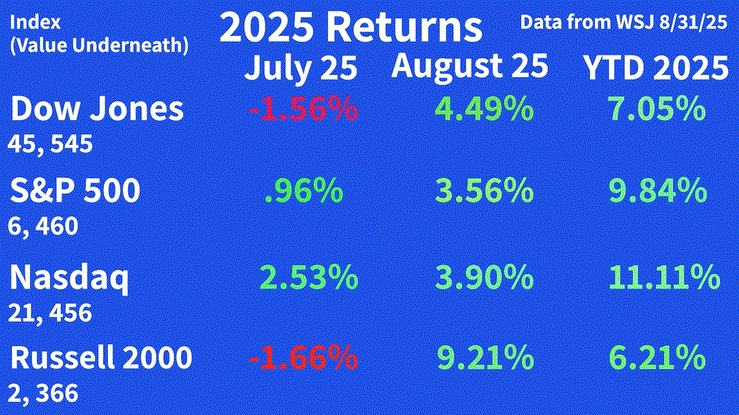

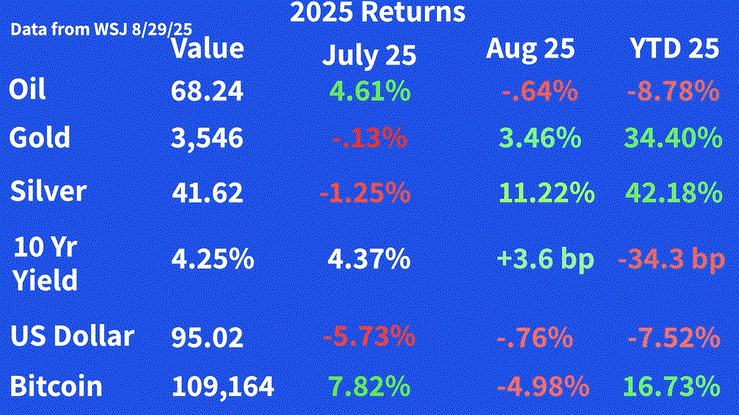

(Return figures come from the August 29, 2025, edition of the Wall St. Journal. Y H & C Investments may have positions in companies mentioned in this newsletter. Nothing in the newsletter should be taken as an offer to buy or sell individual securities. It is the responsibility of each investor to research the investments mentioned so they can decide on the appropriateness and suitability of the investments consistent with their risk tolerance, risk constraints, and return objectives)

When you start out in education, you are taught the grading scale. A means excellent work or outstanding. D or F represents poor performance or failing. An additional category is for behavior. These classifications are E for excellent, S for satisfactory, or U for unsatisfactory. Generally speaking, people across the globe understand A is for excellence, F is for failure.

Capital markets have their own version of grading scales, and it is especially important when it comes to analyzing and evaluating assets. A few quick basics to get started. When a company raises capital in the equity market, it issues shares. If it issues 1 million shares at 10 dollars a share, that means it raises 10 million dollars. It can also issue debt through notes or bonds, which means it will have to pay interest on the debt to the owners of the debt obligations. By issuing shares or debt, an enterprise increases the capital of the business (for shareholders or debt owners, called creditors). When a company buys back stock or debt, it is reducing the number of instruments available (shares outstanding or debt owed). From an owner’s point of view, when a company issues shares, the existing owner now owns less of the company. If the entity buys them back, the current shareholder owns more of the company. Ok, let’s turn to our version of the grading scale, shall we?

When there is a merger or acquisition, a deal is either called accretive or dilutive. Accretive means that the deal is projected to add earnings (profits) on a per share basis. It means each owner will wind up with more profits per share of stock they owned than prior to the deal. As this is a good thing for owners, we will give accretive the A grade. Dilutive means a deal is projected to lower profits on a per share basis. Clearly, this is not a good outcome for existing owners, so we will give this a D grade. One of the classifications for behavior is an S for satisfactory. We are going to use the S to represent the very important concept of scarcity. Scarcity means having a limited amount of something. The easiest way to understand it is there is only one of any individual persons in the world. There are over 8 billion humans on the planet. However, each person is unique. Another example to understand scarcity is real estate. There is only one Empire State Building or Grand Canyon. Ok, now let’s turn to the most prominent situation in the capital markets, what some observers are now hailing as a big comeback.

People love comeback stories. Historically, probably the most famous one is Napolean. Politically, the current comeback kid is our existing President, Donald Trump. Prior to that, Bill Clinton used the line after his second-place finish in the New Hampshire primary vaulted him to the Democratic nomination and the Presidency. Ok, but in the stock market today, the be all and end all of comebacks is now Michael Saylor, the co-founder of Strategy (formerly MicroStrategy-MSTR).

Mr. Saylor founded the software company in 1989 and served as the CEO until 2022. It initially had spectacular success during the dot com period, but the company was accused of accounting misstatements for three years of prior financial filings and the stock plunged, wiping out over $6 billion of Mr. Saylor’s personal value. His comeback involved the asset bitcoin. Let’s briefly return to our grade scale. The whole premise of why Bitcoin is a valuable holding is through the idea of scarcity, S. Published in a white paper by Satoshi Nakamoto in 2008, a key component was there are only 21 million bitcoins across the globe. As we speak today, there are only 19.9 million available. Mr. Saylor decided he would change the direction of Strategy by buying massive amounts of Bitcoin in August 2020. Over the last five years, Strategy has bought over 600 thousand bitcoins. The largest owner is Mr. Nakamoto with over one million coins.

Mr. Saylor applied his own version of creative finance and fundraising by using all kinds of company instruments to purchase Bitcoin. He has issued straight debt, convertible debt, preferred stock, and common stock to raise money, all to buy bitcoin. These capital raises have worked for Mr. Saylor, as the value of bitcoin has risen to over $100K per coin. It has worked so well that the value of the strategy stock was worth double the market value of the coins which Strategy owns (the premium has shrunk). If one wanted to own bitcoin, one could just buy bitcoin or an exchange traded fund that owns bitcoin.

Naturally, Mr. Saylor has received a lot of attention for his success, so much so that there are market participants who are copying his approach by buying other crypto related assets like Ethereum, Ripple, Solana, and the joy that is Hyperliquid. These imitators are called digital holding companies and can be bought on the listed exchanges as well. No, I don’t own any and will not participate. For a more detailed look on this topic, Matt Levine writes an excellent column that might help as well (skip to the part that says Strategy) -Pod Shops Are the New Banks - Bloomberg

My own thinking is this strategy has currently worked as the underlying value of the asset in question has gone up. If, however, it goes down and in size, then all of the instruments which have been issued to buy Bitcoin may at some point have to be converted to stock. Many shares of stock would have to be delivered to cover the loss of value of the underlying holding (Bitcoin). It would mean massive dilution. Remembering our grade scale, the current A grade could very quickly become a D. Time will tell and who knows what would have to transpire for the price of Bitcoin to dramatically fall so much. Potentially, the same thing can happen to the imitators as well. However, the one important point to consider is the underlying idea of scarcity, S. We apply this idea to analyzing companies. The basic premise is choosing entities with capital structures which are advantaged, meaning scarce, so when they prove the merit of the business, as owners of the limited number of shares we benefit. In sum, it is important to understand the fundamentals of any asset to improve the probability of a positive outcome when investing your hard-earned capital.

Spanning the Globe: YPF Ruling Gives Milei More Time, Japan’s Interest Rates, and Vietnam Storms-

(Video is from over 5 years ago so please consider the time and source)

In August, a New York appeals court ruled Argentina does not have to turn over the controlling stake of Argentina based energy firm YPF to holders of a $16 billion judgment. The decision grants Argentina time during the appeals process, which is expected to take months, to evaluate how to pay for this liability. The Vaca Muerte is an oil and gas deposit which is estimated to contain the world’s second largest shale gas reserves and the fourth largest unconventional oil reserves. The Milei government has opened up its development by not restricting capital investment and partnership to Argentina domiciled companies. The major bottleneck for production and growth is the lack of pipelines, export terminals, and storage and processing facilities to support higher production. Estimates of the Vaca Muerte energy possibilities are it being able to supply both Argentina’s and Brazil’s full energy needs. It is not out of the realm of possibilities exports to other parts of South, Central, and North America exist as well. The first partnership infrastructure projects from private capital are scheduled to be completed in 2027. The IMF and Argentina reached a $20 billion, 48-month deal for funding in April of 2025. In July, the initial $2 billion of the funds was approved to be distributed. Argentina needs to rebuild its foreign reserves in order to help continue to lower financing costs and improve credibility with global investors. Over the last few months, the travel season has seen net capital flow out of Argentina, not helping Milei’s efforts. Argentina is scheduled to have national, provincial, and residential elections on October 26, 2025. The outcome will certainly have an effect on Milei’s efforts to revitalize the energy sector and perhaps turn Argentina into an energy power. If the results were to favor Milei, the effect on the western hemisphere, and global energy, could be transformational.

More on Milei’s efforts-Milei Digs In to Defend Argentine Peso Before Midterm Elections - Bloomberg

In Asia, the Bank of Japan is expected to raise interest rates in October by .25% (to .75% from .50%). The timing of Japan’s meeting allows it to see what Jerome and the Fed will do during their meeting in September, probably a twenty-five-basis point cut. Some investors believe the Yen is the key currency to watch across the globe as it is involved in many different funding situations. As an example, if one were to enact the current carry trade by borrowing Yen to invest in dollars, the spread of 3.5% in those currencies probably does not negate the currency risk. If you are interested in a convertible bond strategy, here you go-

Elsewhere, over the weekend, typhoon Kajiki reached land in Vietnam in China. It is causing hundreds of thousands to evacuate and seek secure shelter. Hurrican season typically arrives now in the Gulf of Mexico so let’s hope nothing like Kajiki arrives here in the US.

Y H & C Investments Firm Update-

August is traditionally a volatile month for markets as volumes are much lighter than normal. The increase of merger and acquisition activity is notable as every day it seems a new deal is being announced. Most deals fail to add value for the acquirer, but that also is related to the topic discussed in the first section. In order to add value for shareholders, a company must grow the profits per share of stock of each owner. When one is taught about capital structure, the basic premise is there is no difference between a capital structure of 10 million shares outstanding at $10 per share and 50 million shares outstanding at $2 per share. If one multiplies both, the total value comes to $100 million. Let’s say this the starting point for a company, but with two different approaches. In the first case, the business goes from 50 million in revenue and 5 million in profit to 100 million in revenue and 12 million in profit and does so by not issuing more stock and once every few years buying back 5% of the shares when they are cheap. In the second path, the company has the same results but instead issues 5% per year in stock options and restricted stock awards to management. Over time, the first company sees the shares outstanding go down, so owners are earning more profits per share. The second is adding to the number of shares outstanding and owners wind up with fewer profits per share.

I look for companies with a capital structure and the advantage of scarcity. When the business grows from x to 2x to 3x, the additional size of the business benefits it’s owners. Make no mistake, investors have to see the business grow for value to accrue to shareholders and usually this is the major hurdle management teams have to overcome. However, if one starts with far fewer shares available, and management and other capital providers it is familiar with own a vast majority of the total available, as growth is achieved the existing owner’s benefit. One only needs to look at examples like Berkshire Hathaway, AutoZone, Dillard’s, or Ralph Lauren to see how a limited number of shares combined with a growing company create value for owners. In combination with well-timed buy backs, the results can be astonishing.

As a final point, with many high-tech businesses backed by venture capital firms or large institutions like Vanguard or T. Rowe Price, the IPOs are structured so a small percentage of the total number of shares held by investors actually are part of the IPO process- usually 5-10 percent. It is why you often see these large moves in IPOs on the first day. S is for scarcity.

Conversely, what we often see, especially in small and micro-cap land, is value destruction. The underlying business starts with capital structures which have a great many shares. The business does not grow. Management issues itself more options over time. Management issues stock at the bottom of a poor period for the business, diluting owners. Rinse. Repeat. Destroy value. Thanks, but no thanks.

Turning to our holdings, earnings season was interesting in that quite a few companies reported numbers which were in line with what was expected. Naturally, there are always a few reports which leave one a little miffed. Investor reaction to the reports has been quite harsh as one common pattern is buy the rumor, sell the news. The stock runs up a little before the report and then is sold after the numbers are released. Trading volumes go up dramatically around the report, and a few weeks later, the stock recovers its losses. Long term owners should understand that over time, a profitable company which adds cash to the balance sheet on a consistent basis is eventually going to be in a position to create value. The priority is to reinvest in the business. It also might use the cash to buy back shares. It might retire or refinance debt. It may make an acquisition. Many of our holdings, especially smaller ones, have been buying their own shares back. Quite a few are actively looking for acquisition candidates. Over time, and it can be years and years, eventually owners can benefit.

Interactive Advisors GARP Models

I thought I would mention what is transpiring for those readers who are invested in the Interactive Advisor GARP Models. In the Long Term GARP Model, the main holding reported results, and they were excellent, but the stock sold off. The company, a leader in its industry, still has a low penetration rate relative to the total addressable market, so we are not selling even though it did not help our model performance.

With the Long Term GARP Concentrated model, I sold some of our second largest holding to diversify into a few other situations. The model is still quite concentrated, and the new positions are businesses I feel have excellent chances to provide diversification and improved growth but with fundamentally solid enterprises. Finally, with the help of the wonderful Sean Aronson, we added a new simulator to my web site for investors to work with in evaluating these models- you might take a look here-

And yes, the models-

Y H & C Investments: Concentrated GARP Investment Portfolio - Interactive Advisors

Y H & C Investments: Long Term GARP Investment Portfolio - Interactive Advisors

Thank you for reading the September update, I really appreciate it. If you have any investment questions, please reach out to me at information@y-hc.com.

(Y H & C Investments may have positions in companies mentioned in this newsletter. Nothing in the newsletter should be taken as an offer to buy or sell individual securities. It is the responsibility of each investor to research the investments mentioned so they can decide on the appropriateness and suitability of the investments consistent with their risk tolerance, risk constraints, and return objectives)

.png)